Results at a glance

The Positive

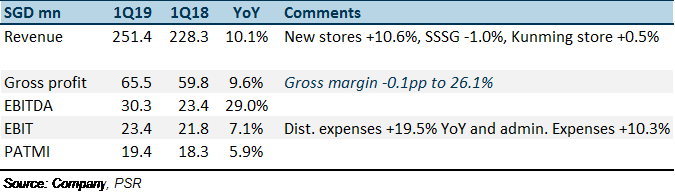

+ Sales growth was healthy. 1Q19 sales growth of 10.1% YoY was above our modelled 7%. Growth was supported purely by the new stores as same-store sales contracted 1% YoY.

+ Three new stores secured. In May 2019, Sheng Siong secured 3 new stores (or 15,780 sft). This will boost total store footprint by 3%. These three stores are close-bid stores retendered from existing sites that were given up. Another six new stores have recently been tendered out by HDB. These stores may include non-price factors as part of the requirements.

The Negative

– Same-store sales a worry. As per the previous quarter, same-store sales is the weak spot. It contracted 1% during the quarter. This is comparable to the almost 2% same-store sales decline recorded by supermarkets located within retail malls*.

– Operating expenses trended higher. 1Q19 operating expenses was 17.7% of sales, marginally higher than our modelled 17.5%. New stores will require time to scale up. According to the company, gross margins were a tad lower due to the timing of rebates. Contribution of fresh products to the sales mix was in fact higher YoY in 1Q19.

*Using data from CapitaLand Mall Trust 1Q19 presentation as a proxy.

Outlook

In spite of the weak consumer sentiment, Sheng Siong has been raising their market share of supermarket sales. Supermarket sales in Singapore contracted almost 2% year-to-date, as at end-Feb 2019. Sheng Siong would have captured market share with their 10% jump in sales. We are still positive on the outlook. The almost 11% growth in retail space for 2019 will help support growth. Another growth driver will be the higher sales per square feet.

Upgrade to BUY with unchanged TP of S$1.30.

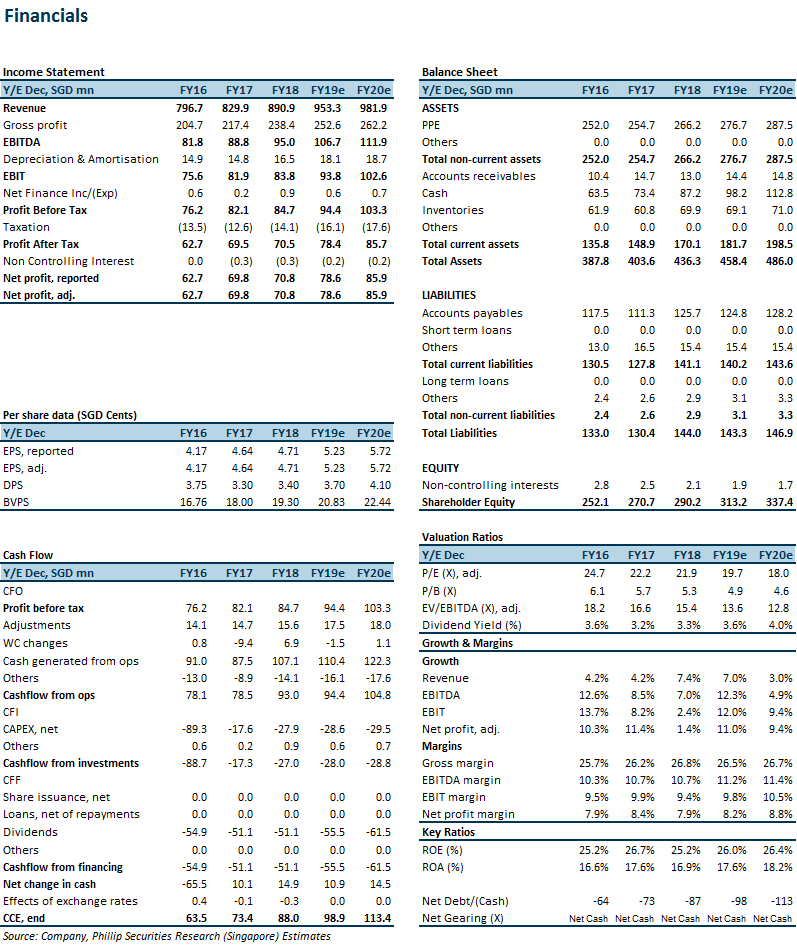

Our TP is based on an estimated 25x PE multiple. The company is expanding its store count, increasing market share and currently offers a 25% ROE with a S$87mn net cash balance sheet.

Paul has 20 years of experience as a fund manager and sell-side analyst. During his time as fund manager, he has managed multiple funds and mandates including capital guaranteed, dividend income, renewable energy, single country and regionally focused funds.

He graduated from Monash University and had completed both his Chartered Financial Analyst and Australian CPA programme.