The Positives

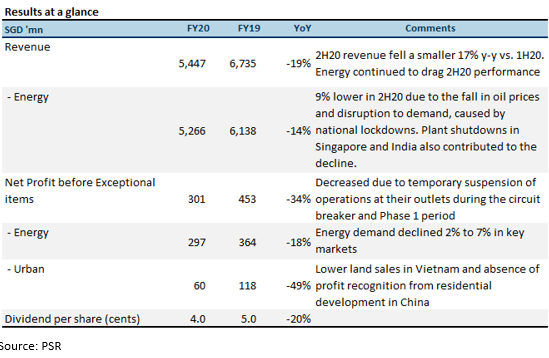

+ Net profit before EI ahead of our expectation. Higher energy demand in 2H20 brought group net profit before EI to S$301mn, beating our estimate for a S$147mn loss. Supported by its underlying profitability, the group proposed a final dividend of 4.0 Singapore cents. Without the encumbrance of the Marine business, we expect the Company to be able to support increased payouts going forward.

+ Energy demand recovered slightly. Energy demand and prices improved sequentially in 4Q20 in its key operating markets, Singapore, China and India. As lockdowns ease in these markets, we believe demand can further recover in FY21e. Amid a challenging macro environment, its Energy and Urban businesses were resilient. The Group continued to deliver positive operating cash flow.

+ Myanmar operations unaffected. Through its subsidiary, Sembcorp Myingyan Power Company Limited, Sembcorp operates a 225-megawatt gas-fired power plant in Mandalay, Myanmar. The plant continues to be in operation and there have been no disruptions.

The Negative

– Earnings of about S$30mn at risk. The potential exit of a major customer on Jurong Island in 2021 and a 1-year overhaul of a customer’s facilities in the UK may affect the Energy segment this year. In 2020, these customers contributed about S$30mn of net profits in total.

– Impairments of S$261mn recorded for FY20. The Group recognised S$261mn in impairments for FY20, which had a negative impact on their equity value. These comprised of S$81mn and S$32m impairments in investments in Sembcorp Salalah Power and Water Company and CSE of respectively. We do not expect any further impairments for FY21e and FY22e.

Outlook

Despite persistent uncertainties surrounding recovery from the COVID-19 pandemic, we remain positive on the Group’s outlook as energy demand is recovering in its key operating markets. We expect the Group to continue transiting its portfolio to sustainable solutions and sustainable development. In 2021, about 200MW of renewable-energy capacity is expected to come onstream.

Downgrade to ACCUMULATE, albeit with higher target price of S$1.77

Recent share-price rally has moved SCI to 0.6x FY21e P/B. We raise our target price to S$1.77 from S$1.75 as we now peg SCI to 0.85x FY21e P/B, closer to their 10-year historical average P/B, up from 0.7x previously. This reflects its improving outlook and stronger operating metrics expected for FY21e. However, as most of its positives have been priced in, downgrade from BUY to ACCUMULATE.

Terence specialises in the consumer, conglomerate and industrials sector. He has over five years of experience as an analyst in the buy- and sell-side. As an institutional fund management analyst, he sat on the China-Hong Kong desk. Terence was ranked top 3 for Best Analyst under the small caps and energy category in the Asia Money poll 2018.

He graduated from the Singapore Management University with a major in Finance (Honours), and is the honoured recipient of the CFA scholarship.