The Positive

+ Higher local patient load and rental income mitigated weaker healthcare services segment. Its insurance business (contributing <10% of Healthcare services Revenue) was hit by lower renewal of international healthcare plans for expatriates, particularly from the financial sector. Strong local demand underpinned growth amidst plateaued foreign patient volume growth.

Raffles Holland V is now fully leased with around 4.7% net rental yield. Note that it only recorded one quarter of rental income in FY17 (upon the end of one-year rental-free provision); we would see a higher rental income in FY18 due to a full year contribution from Raffles Holland V.

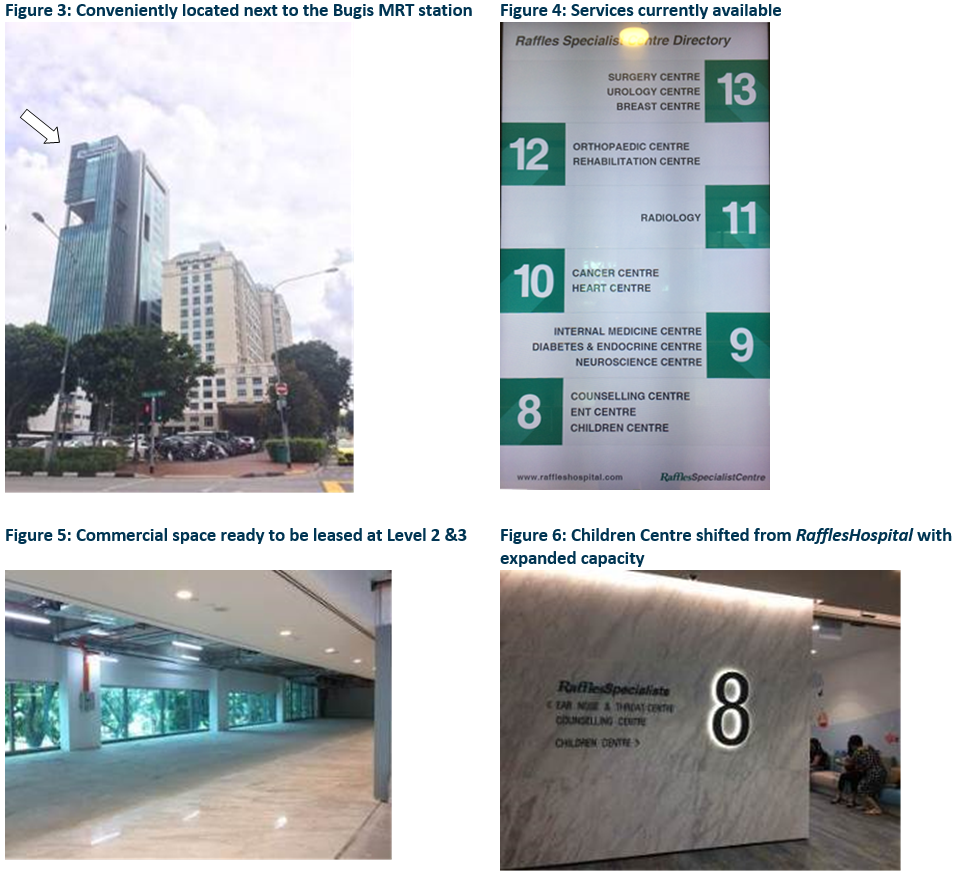

+ Expanded capacity in RafflesHospital and RafflesSpecialistCentre to cater for the growing local and foreign demand. The new RafflesSpecialistCentre (RafflesHospital’s extension) has commenced operation since 22 Jan-18.

Various specialist centres and the radiology centre have been relocated to the new building from RafflesHospital. Meanwhile, RafflesHospital is undergoing construction to open up new wards to increase bed capacity, as well as to refurbish the podium for new commercial outlets. The construction is slated for completion by end May-18.

The Negative

– Staff costs to remain elevated as the Group gears up for the two new hospitals in China. We expect staff costs to stay above 50% of Group’s revenue in coming years until patient volume picks up in RafflesSpecialistCentre, MCH (MC Holdings) and the two new hospitals in China.

Outlook

Outlook remains positive despite medium-term margin pressures from higher staff costs and start-up costs from the gestation of its two new China hospitals.

Maintained Accumulate with unchanged TP of S$1.32

We remain upbeat on the potential growth that these new hospitals in China would bring to the Group: (i) Diversification with a higher contribution for overseas operation; and (ii) Tapping into China’s growth.

Potential re-rating catalysts:

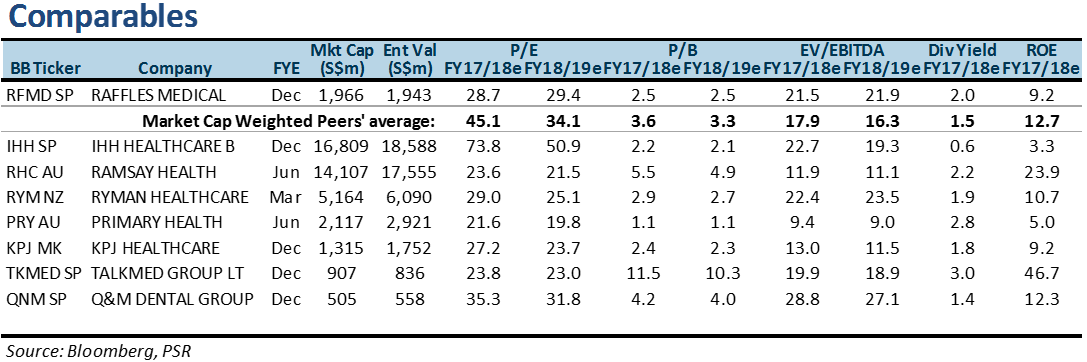

Figure 2: Peers Comparison

Raffles Medical Group is currently trading at 28.7x forward PER, which is a 36.4% discount to its regional peers’ average of 45.1x.

Its FY18e dividend yield of 2.0% is 33.3% higher than its regional peers’ average.

A Sneak Preview of the new RafflesSpecialistCentre

Lin Sin has been an investment analyst in Phillip Securities Research since June 2014, where she started as an economist, focusing on China and ASEAN macroeconomics. Currently, she covers primarily the Consumers and Healthcare sectors in Singapore equities market.

She graduated with a Bachelor of Science in Mathematics and Economics from NTU.