The Positives

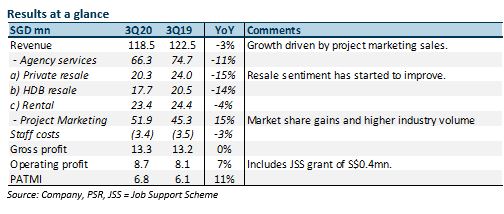

+ Project marketing resilient. 2Q20 new home sales for the industry were down 27% YoY. We had expected the weakness to spill into this quarter as there is usually a lag of 2-3 months before revenue is billable. PropNex was resilient due to market-share gains, delays in prior sales due to options re-issuance and its ability to market projects virtually.

+ Cash kept piling up. 9M20 operating cash flow was S$30mn (9M19: S$21mn). As capex was minimal at S$0.2mn, cash buffer should be sufficient to meet our dividend forecast of S$14.8mn (DPU of 4 cents).

The Negative

– Nil.

Outlook

Resale volumes are recovering as consumer sentiment improves. HDB resales should be supported by enhanced grants for HBD purchasers introduced late last year and delays in BTO completions. Meanwhile, project sales could enter a near-term lull in October and November due to delays in new launches. In September, URA had restricted developers from re-issuing options. Potential buyers will likely need greater clarity and time before disposing of their existing properties and committing to new purchases.

Maintain BUY with higher TP of S$0.85, up from S$0.70

We raise our TP as FY20e/FY21e earnings have been increased by 40%/46% to factor in stronger than expected new-project revenue.

Paul has 20 years of experience as a fund manager and sell-side analyst. During his time as fund manager, he has managed multiple funds and mandates including capital guaranteed, dividend income, renewable energy, single country and regionally focused funds.

He graduated from Monash University and had completed both his Chartered Financial Analyst and Australian CPA programme.