The Positives

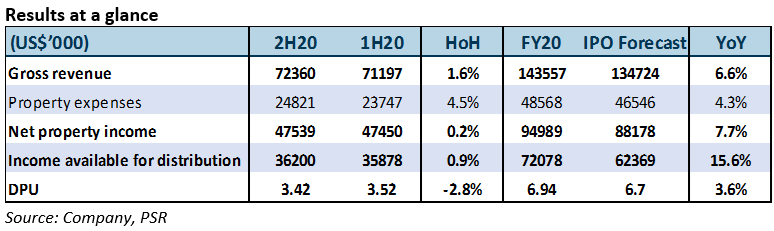

+ Outperformed FY20 NPI target by 7.7%, DPU by 3.6%. Notwithstanding the pandemic, Prime’s income was resilient. Rent collection was 99% throughout FY20 with minimal deferrals granted to tenants. HoH, performance was stable. FY20 gross revenue and NPI were 6.6% above IPO forecasts largely due to contributions from Park Tower acquired in February 2020. Distributable income was 15.6% higher than IPO forecast, attributable to lower trust, finance and tax expenses. FY20 DPU was at 96% of expectations.

+ Strong leasing with minimal expiries in FY21. In FY20, Prime signed 225k sq ft of leases at positive rental reversions of 7.2%. More than 60% were renewals or for expansion by existing tenants. New tenants were from established and technology sectors, including Northwestern Mutual, Towers Watson and Washington University. Leases due to expire in FY21 account for only 8.8% of cash rental income (CRI). These expiries are well spread across its properties with none above 1.5%. Month to month leases constitute 1.1% of CRI.

+ Stable portfolio valuation despite Covid-19. Valuers have kept cap and discount rates similar to prior years, as transactions in the office market have been fewer. Main variables were rent and occupancy assumptions. Timings of lease expiries, probability of roll-overs and renewals were accounted for. Valuations for Tower I at Emeryville and Promenade I & II declined the most, by 8% and 5.3% respectively. This was offset by higher valuations for Village Centre II and 222 Main, Prime’s biggest assets. As a result, portfolio valuations dipped by less than 1%, underscoring the strength of Prime’s diversification.

The Negative

– Vacancies at Village Center Station I and 171 17th Street yet to be filled. Portfolio occupancy was stable at 92.4% vs. 3Q20’s 92.6%. Only Village Center Station I and 171 17th Street have been operating at below-portfolio occupancies of 65% and 86% since 1H20. The properties contribute 4.3% and 12.9% to portfolio NPI respectively. Although leasing has not stalled in both markets, these two properties have not been benefitting from this. We believe this is due to longer periods of decision making as both properties are still seeing enquiries from prospective tenants. We lower our FY21 occupancy forecasts for both by 8% and 4% respectively.