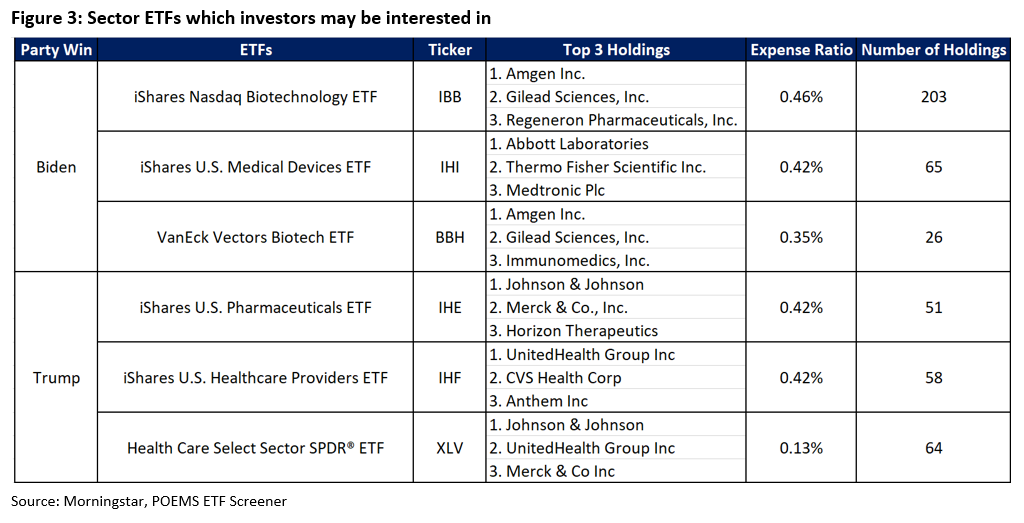

Introduction

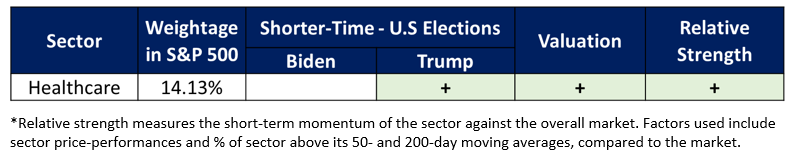

The healthcare sector consists of companies which provide medical services, medical equipment, drugs and medical insurance. It accounts for close to a fifth of U.S. GDP. Drug manufacturers make up the majority 37.7% of the sector. Other players include biotechnology firms and healthcare insurance providers, which account for 14.4% and 9.8% respectively.

Fundamentals

Covid-19 has had a mixed impact on the healthcare sector. Biotechnology and pharmaceutical companies may stand to benefit if they produce tests and vaccines for Covid-19. At the other end of the spectrum, the crisis has delayed elective surgeries and reduced visits to doctors for non-urgent treatment. A recent spike in Covid-19 cases may prompt states to reimpose elective surgery restrictions. Therefore, we believe that companies which do not have a foot in Covid-related development may continue to face headwinds. For insurers, massive unemployment may lead to cutbacks in insurance premiums. However, with the continued recovery in the labour market and potential fiscal stimulus, we believe the impact will be short-lived.

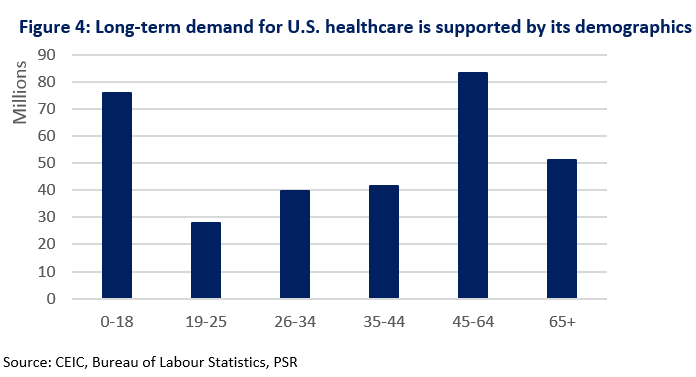

Longer term, demand for healthcare should remain anchored by an ageing population. Baby boomers – aged 65 and above – account for 16% of the U.S. population. The next age band of 45-64 years old accounts for 26% (Figure 4). These demographics should provide a steady stream of demand for pharmaceutical drugs and healthcare services over the next 10-20 years. Low interest rates, we believe, will support M&As by the huge pharmaceutical companies to gain access to new products.

U.S Elections – Policy Overview

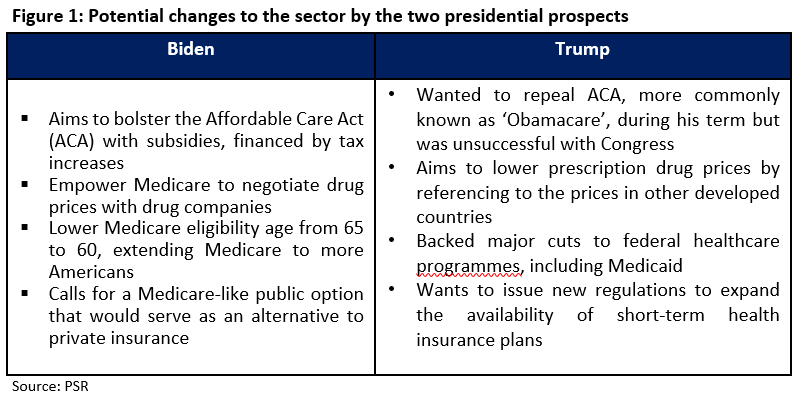

Covid-19 has intensified the spotlight on the healthcare policies of Biden and Trump. We provide an overview of their proposed polices in Figure 1.

Potential impact on healthcare sector under different scenarios

Healthcare policies have always been tricky. There tend to be starkly different views on the trade-off between providing affordable healthcare to consumers and supporting the healthcare industries. Therefore, the composition of the new Congress matters as a unified government may increase the chances of pushing out aggressive policies. A split Congress may result in a stalemate, which generally favours the healthcare companies.

Sector Outlook

Private Insurers

We believe Trump may be positive for insurers. He is determined to weaken the ACA, which has various restrictions on insurers such as covering pre-existing conditions and no coverage limit. Further deregulation may increase flexibility for insurers and give them better control of premiums. Biden’s proposed policies could be mixed for insurers. Although he seeks to extend Medicare and Medicaid to more Americans, he is eyeing a government-run public option as an alternative for private insurance. We believe more clarity is needed as his ideas are still in the formation stage. The outlook for private insurers is thus highly uncertain.

Pharmaceuticals/Biotechnology

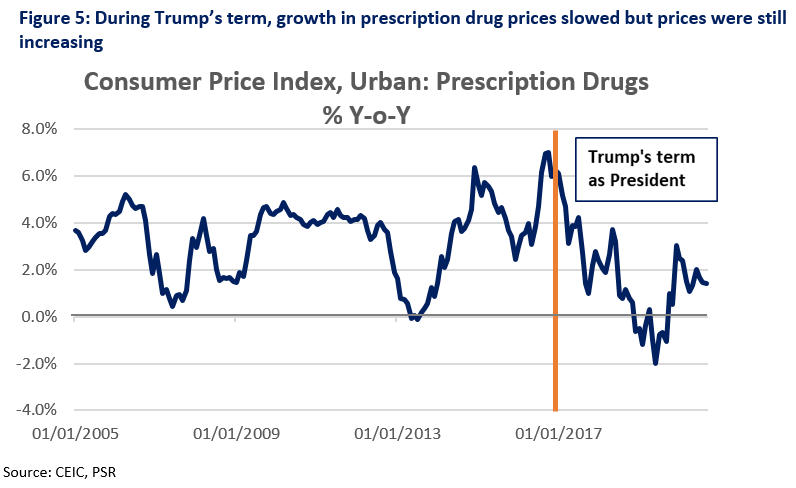

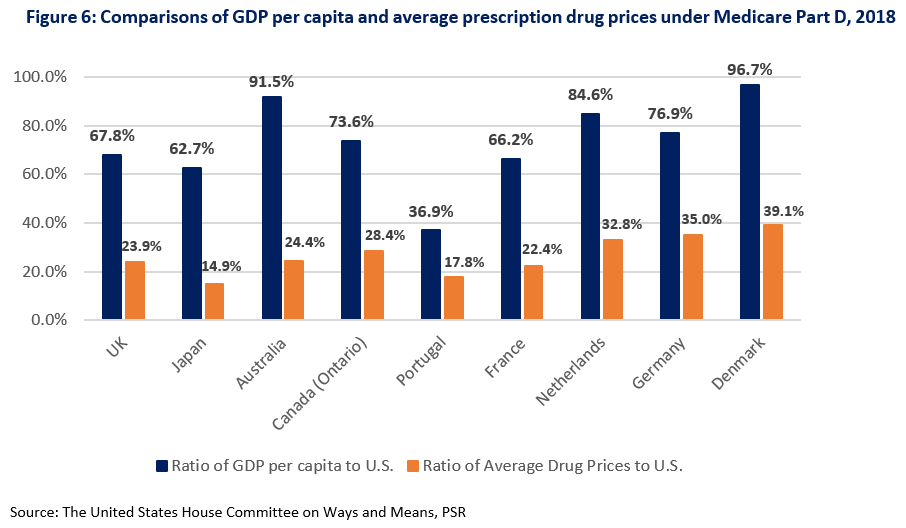

Both Biden and Trump aim to lower drug prices to make healthcare more affordable, but Biden is expected to have a greater chance of success. During Trump’s term, drug prices continued to grow y-o-y at around 2% (Figure 5). We believe his proposal to benchmark prices to those in the other countries is not feasible. Average prescription drug prices in the other developed countries stood at 15-40% of U.S. drug prices in 2018 (Figure 6). The trade-off will require either a high rebate rate of 60-70% from insurers or a 60% fall in revenue for drug manufacturers, both of which will be fiercely resisted by the industries. His previous attempt at reducing prices were also unsuccessful and we believe drug prices will continue to climb under his re-election.

Biden aims to allow Medicare to negotiate for lower drug prices with pharmaceutical companies. His success will depend on the leverage used to compel a company to provide competitive prices. However, we see greater chances of success in this ‘hard’ approach than Trump’s, as Medicare, being administered by a federal agency, may take tougher actions against companies for non-compliance.

The biotechnology industry may not be spared from the clampdown on drug pricing, though near-term opportunities remain. A Biden win will likely see a ramp-up of Covid testing. Investments in vaccine manufacturing should also continue, regardless of who becomes President. Therefore, biotechnology firms with Covid-related exposure should benefit in the near term.

Healthcare equipment makers

Biden aims to manufacture more medical equipment and other critical supplies to battle future pandemics and avoid reliance on other countries’ supplies. This bodes well for domestic equipment makers who may ramp up production. Trump hopes to boost domestic manufacturing but has not flagged healthcare equipment specifically.

Healthcare service providers

We believe healthcare service providers will benefit either which way, more so under Biden. Biden aims to expand Medicare and Medicaid to more Americans, which should lift demand for healthcare services. His plan to increase cost-sharing reductions for middle-class Americans may also lead to higher adoption of healthcare services. Trump aims to promote telehealth services to expand healthcare access to rural areas and Medicare. Therefore, providers with telehealth growth may see greater demand for their services.

Valuation/ Relative Strength

Current forward P/E ratio for the healthcare sector stands at 17.8x. This is below its 5-year historical average of 20.4x. Forward dividend yield stands at 1.68%, which is in line with its 5-year average of 1.66%. This indicates the sector is more of a growth than dividend play. Its performance has been roughly in line with the market. About 69.8% of S&P 500 healthcare stocks are trading above their 200-day moving averages, close to the 68.9% for the S&P 500.

RECOMMENDATION:

We believe future healthcare policies are intertwined closely with the composition of the new Congress. A divided Congress will likely push out big legislation and we may end up with little or no structural change. This would remove uncertainty for the sector and would be seen as largely positive. If a Blue Wave occurs, Biden’s ambition to remake the healthcare system may be more likely to pass. However, we believe that the near-term focus will still be on Covid-19 and any regulation or major changes may be put on hold until the worst of the crisis is over. Therefore, we do not expect any significant overhaul of the system over the next 1-2 years. Under both candidates, healthcare adoption may rise, but potentially more so under Biden due to his plans to get more people insured.