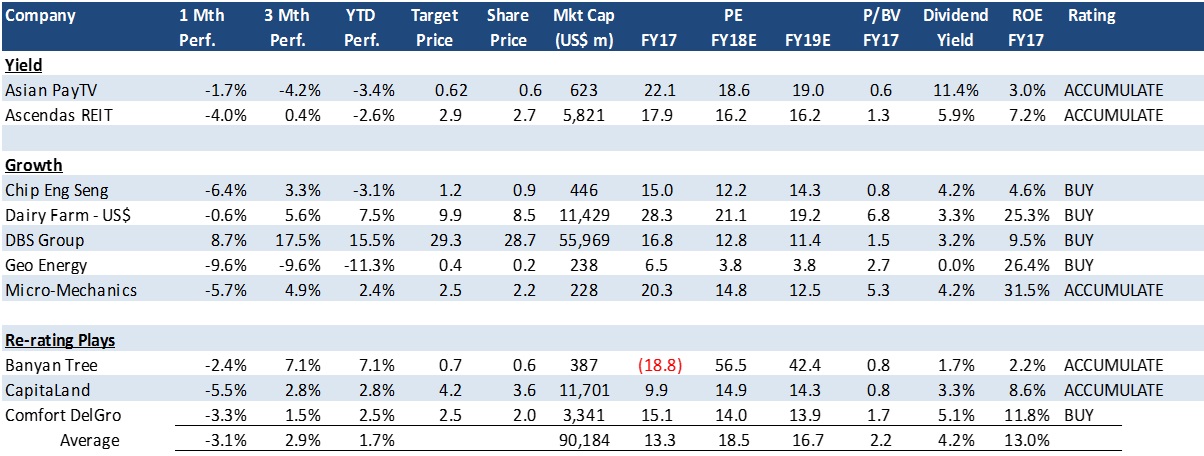

PHILLIP ABSOLUTE 10 – Our top 10 picks for absolute returns

Source: Bloomberg, PSR

Phillip Absolute 10 performance assumes equal weightage to every stock in the portfolio. Any changes to Phillip portfolio is only conducted month end.

In our inaugural Phillip Absolute 10 Model portfolio, it was up 4.9% in January. It outperformed the STI by 1% point. Our portfolio underperformed this month, hurt by the performance of Geo Energy, Chip Eng Seng and Micro-Mechanics. Only DBS managed to generate positive gains for us in February. Our portfolio for March will exit DBS and replace it with OCBC.

Below are some quick updates on some of the Absolute 10 portfolio:

OCBC: We will be removing DBS and replacing with OCBC. Due to the outperformance in DBS, we believe OCBC will be a better proxy to banking sector. OCBC will enjoy the upside in interest rates through the insurance arm and leveraged on the rebound in credit cycle in both Singapore and Hong Kong.

Geo Energy: Share price has suffered due to weak production in 4Q17 and regulatory noise out of Indonesia. We still like the stock for the attractive valuations, growth in production and healthy coal prices.

Chip Eng Seng: We maintain our Accumulate call on CES with unchanged target price as we see strong revenue visibility for FY18/19 with an estimated $210mn of unbooked development profits from High Park and Grandeur Park Residences. The improving hospitality and construction segments will continue to support recurring income. The Group’s recent announcement to diversify into the Education sector remains a mid-long term goal. We will update accordingly, when there is more clarity. Dividend yield, which we expect to be maintained, is at an attractive >4% level, and target price is at a steep 40% discount to RNAV.

Micro-Mechanics: Whilst the results reflected some weakening in momentum, we still are upbeat on the company. The attractive investment merits of Micro-Mechanics have not changed: ROE of >30%, ~60% GP margins, net cash $22mn balance sheet and 3% dividend yield.

Dairy Farm: Most of its segments and its two key associates returned strong performances, while we saw persistent weakness in SE Asia. We like Dairy Farm on its well-established regional presence and solid financial positions. Near-term catalysts include recovery in SE Asia consumer sentiment as well as higher Chinese tourist arrivals to Hong Kong and Macau; increasing online and offline network; and margin gains via better sales mix and economies of scale.

Banyan Tree: We maintain our Accumulate call on BTH with unchanged target price as FY17 results continue to show improved operating performance across its key markets, with the exception of Maldives. RevPAR for Thailand, which accounts for close to 60% of Group revenue by our estimates, jumped c.13% on average for FY17. We expect this strength to continue, especially with the low base in 1H17, after the King is passing. Forward indicators also reflect a more favourable outlook across all business segments as hotel forward bookings jump 15% YoY for 1Q18. The Group’s general offer for Laguna Resorts & Hotel reflects a potential greater sense of urgency to monetize/ develop the existing land bank, which could be further catalysts to share price.

For the full Singapore Monthly for March 2018 report.