|

Review: STI recovered in 2021, rising 9.8% (2020: -11.8%). All the gains came from the banks. DBS alone accounted for around 60% of the rise in STI. Removal of dividend caps and better asset quality provided a re-rating catalyst and an earnings recovery for the banks. Only one-third of the STI component stocks enjoyed gains this year. Outlook: We worry equities may struggle in 1H22. A stagflation head fake of slower economic growth and rising inflation will worry investors. Global growth faces a near-term risk from Omicron concerns and renewed lockdowns. The yield curve is flattening with expectations of slower growth. PMIs and industrial commodities are rolling over. Even with slower growth, interest rates are expected to rise. This follows the Fed’s hawkish pivot. Futures market is pricing three rate hikes by December 2022. After this period of volatility, we expect equities to recover in 2H22. Driving the rally will be the next two tapers. Nope, not the Fed taper. The first taper will be a decline in infections. Omicron is more contagious but early indications suggest less deadly. In South Africa, where Omicron accounts for 98% of all COVID-19 cases, infections underwent a parabolic rise but mortality rates were stable. The situation in the UK mirrors this, where even hospitalization numbers are low. The current pandemic scenario is unlike the 2020 abyss. We have mass vaccinations, including for the children, and anti-viral drugs being introduced. After this terrible wave, our base case is a major tapering off in cases. The next taper will be inflation. Supply bottlenecks will persist with the current lockdowns worsening. But we believe supply constraints and inflation have peaked but not normalised. Freight rates are starting to roll over. Semiconductor capacity is responding to the shortage with a US$240bn spending in foundry capex over two years, a 40% jump. Recommendation: We are positive on building materials, consumer and services. We expect construction to recover sharply with the return of the foreign workforce. The industry has lost 67,000 workers since the pandemic. Beneficiaries of the rebound in construction are building material stocks Pan-United and BRC Asia. Consumer names such as Dairy Farm and Thai Beverage have suffered due to severe lockdowns across SE Asia in 2021. As cases start to drop and lockdowns ease, earnings can normalise against a weak base year. Our preference in the consumer sector is Del Monte. US operations are turning around with new products, higher product prices and restructuring of sales channels and factories. Balance sheet improvement is a bonus. We remain positive on the recovery theme. Our preference includes Ascott Residence Trust. We expect borders to re-open further after the current wave of infections. Hospitality to gain from pent-up demand. ComfortDelgro has disappointed with lockdowns, taxi rebates and poor rail traffic. The stock is 41% below pre-pandemic levels but free cash flow has risen around $400mn over the past two years. In the services sectors, HRnetGroup will benefit from record job vacancies for permanent and flexible staffing. We expect volume and pricing growth to fuel bumper earnings in the coming year.

|

|

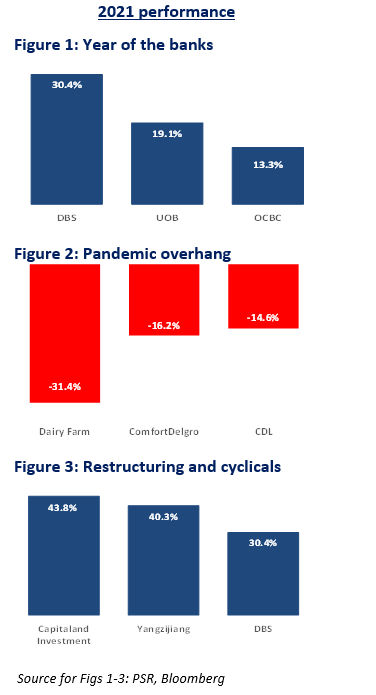

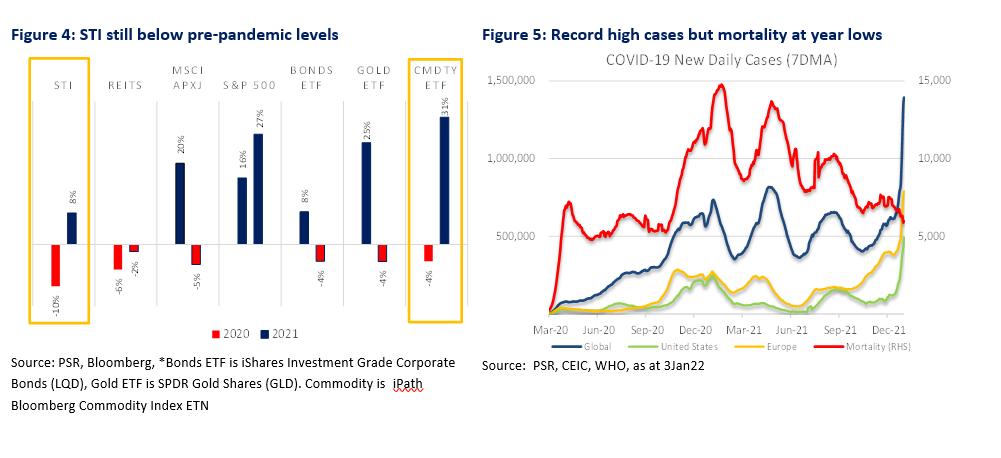

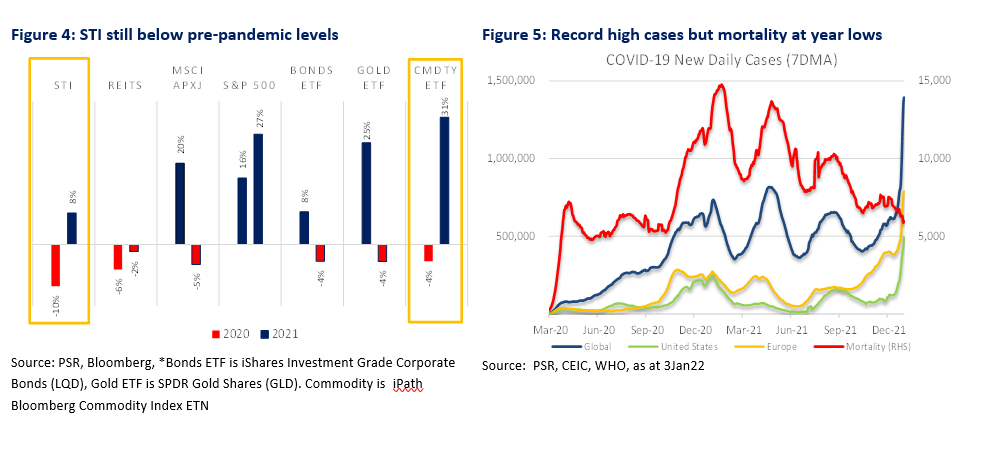

2021 REVIEW STI recovered in 2021, rising 9.8% (2020: -11.8%). All the gains came from the banks (Figure 1). DBS alone accounted for around 60% of the rise in STI. Removal of dividend caps and better asset quality provided a re-rating catalyst and an earnings recovery for the banks. Only one-third of the STI component stocks enjoyed gains this year. Deep cyclicals Yangzijiang and corporate restructurings CapitaLand Investment were the other gainers (Figure 2). Lockdowns and movement restrictions hurt Dairy Farm and ComfortDelgro (Figure 3). Compared to other asset classes, STI is up 7.7% (USD terms), outperforming REITs and Asia Ex-Japan equities (Figure 4) but remains below pre-pandemic levels. US equities registered the 2nd consecutive year of double-digit gains. |

|

OUTLOOK We worry equities may struggle in 1H22. A stagflation head fake of slower economic growth and rising inflation will worry investors. Global growth faces a near-term risk from Omicron concerns and renewed lockdowns (Figure 5). The yield curve is flattening with expectations of slower growth (Figure 6). PMIs and industrial commodities are rolling over. Even with slower growth, interest rates are expected to rise. This follows the Fed’s hawkish pivot. Futures market is pricing three rate hikes by December 2022 (Figure 7). After this period of volatility, we expect equities to recover in 2H22. Driving the rally will be the next two tapers. Nope, not the Fed taper. The first taper will be a decline in infections. Omicron is more contagious but early indications suggest less deadly. In South Africa, where Omicron accounts for 98% of all COVID-19 cases, infections underwent a parabolic rise but mortality rates were stable (Figure 8). The situation in the UK mirrors this, where even hospitalization numbers are low. The current pandemic scenario is unlike the 2020 abyss. We have mass vaccinations, including for the children, and anti-viral drugs are being introduced. After this terrible wave, our base case is a major tapering off in cases. Ironically, immunity from infection is building up with Omicron. The next taper will be inflation. Supply bottlenecks will persist with the current lockdowns worsening. But we believe supply constraints and inflation have peaked but not normalised. Freight rates are starting to roll over (Figure 10). Semiconductor capacity is responding to the shortage with a US$240bn spending in foundry capex over two years, a 40% jump (Figure 11). Companies have started to get accustomed to the tight supply chain and long lead times. |

Paul has 20 years of experience as a fund manager and sell-side analyst. During his time as fund manager, he has managed multiple funds and mandates including capital guaranteed, dividend income, renewable energy, single country and regionally focused funds.

He graduated from Monash University and had completed both his Chartered Financial Analyst and Australian CPA programme.