This report is part of the Phillip 2018 Singapore Strategy Report.

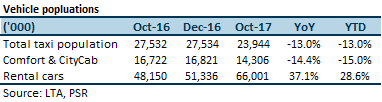

2017 Review The sector’s financial performance was bolstered by the Public Transport Services segment, with SMRT Buses, a subsidiary of SMRT Corp (not listed) and SBS Transit being beneficiaries of the transition to the government-contracting model for scheduled public bus services. For illustration, SBS Transit’s Public Transport Services (combination of Bus and Rail) reported $17.16mn segment profit for 9M FY17, compared to $152,000 segment profit a year ago. Average daily ridership for Downtown Line (DTL) was 258,000 in 3Q 2017, and the preliminary estimate for 4Q 2017 following the commencement of revenue service for Stage 3 (DTL3) is 420,000. LTA projects a steady-state average daily ridership of 500,000. Taxi business model remains under threat by competition from ride-hailing apps. Comparison against total taxi population indicates that Comfort & CityCab has lost market share on a YoY and YTD basis. Rental cars population growth rate has peaked and stagnated from mid-2016 to mid-2017, and has since moderated downwards, refer Figure 72.

Figure 72: Rental cars taking share from taxis

|

Richard covers the Transport Sector and Industrial REITs. He graduated with a Master of Science in Applied Finance from the Singapore Management University. He holds the CFTe and FRM certifications and is a CFA charterholder.

He was ranked #2 Top Stock Picker (Asia) for Real Estate Investment Trusts in the 2018 Thomson Reuters Analyst Awards, and ranked #2 Top Stock Picker (Singapore) for Resources & Infrastructure in the 2016 Thomson Reuters Analyst Awards.