This report is part of the Phillip 2018 Singapore Strategy Report.

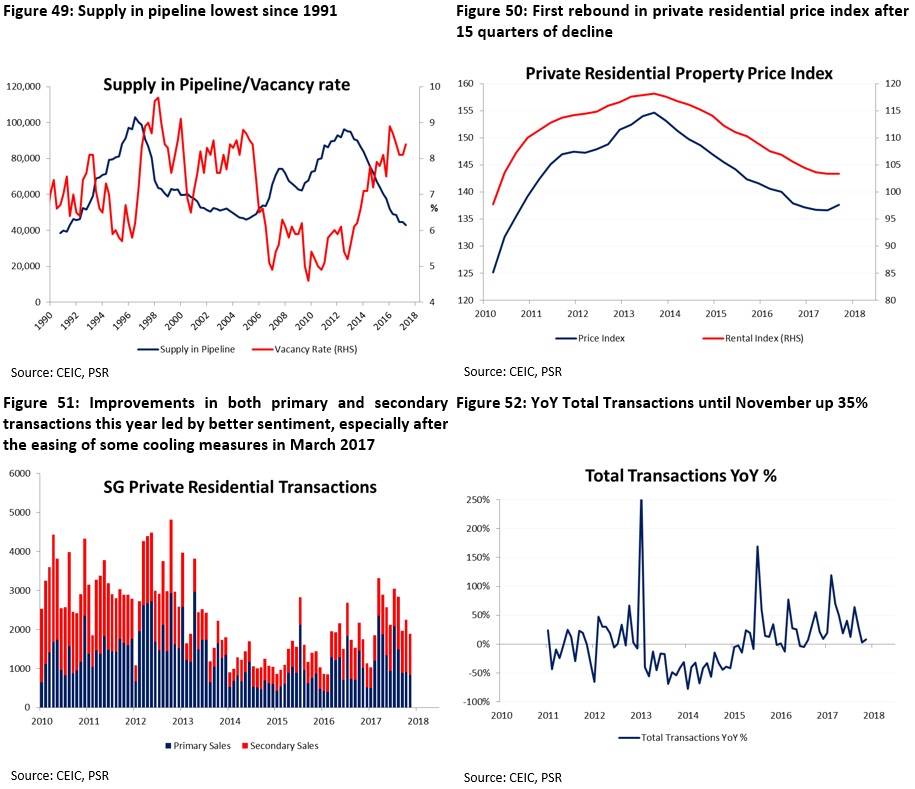

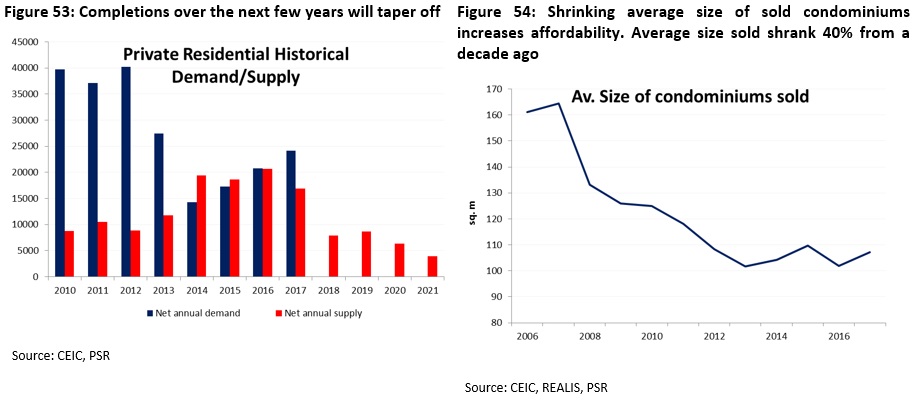

2017 Review Singapore developers returned a strong 30.4% (inclusive of dividends) as at end November 2017, making it the third-best performing. Sentiment was lifted when the government announced in March 2017 the easing of certain cooling measures such as the reduction of Sellers’ Stamp Duty. Improved sentiment, together with strengthening economic conditions, drove transaction volumes higher by 35% YoY to 25,770 units by end Nov 2017 (Figures 51 and 52), the best performance since 2013. The competitive banking landscape saw more banks such as HSBC and UOB join in the fray with attractive 3-year fixed rate mortgages at 1.68%. Ironically, these fixed rates are now lower than 3 years ago when the Fed started hiking rates. Home prices rose 0.5% in 3Q17, the first rise after 15 consecutive quarters of decline (Figure 50). 2017 also saw a series of record high prices for land tenders (GLS/en blocs). For office, Guocoland paid a record land price of S$1,706/psf for Beach Road GLS site, while City Developments’ S$907mn en bloc of Amber Park was Singapore’s largest freehold collective sale by dollar value. En bloc transactions reached S$6.8bn, highest since 2007 (S$12bn). Outlook We expect transaction volumes to maintain their strong momentum into 2018, led by a higher number of new launches. In tandem with higher transaction volumes, we expect private residential prices to rise between 5%-10% in 2018. This will be driven by: Rising affordability as unit sizes shrink (which offsets the impact of higher selling prices $/psf). Average size of all condominium units sold in 2016 shrank c.40% to 100sqm from a decade ago (Figure 54). Along with better demand from improved sentiment and affordability, total supply in pipeline dropped to lowest since 1991, at c.43,054 units (Figure 49). Comparing this to the average annual demand over the last 7 years since post-GFC of c.28,000, existing pipeline supply could be sold out in just 1.5 years. Total en bloc sales since 2016 could add a further 12,000 units of supply. Improved household balance sheet built up from rising equity as a result of strong price appreciation of HDBs in the past decade. Total household mortgage to total asset value dropped from 32% in 2005 to the current c.27%. We expect forward population growth to improve over the 0% growth in FY17 as SG economy improves, and demand for workers rise amidst the low unemployment rate. However, we do not expect this figure to surpass the average +1.2% from 2014-16. Improving rental market over the next couple of years because of low completion numbers and improving demand, (Figure 53) could be further catalyst for home prices. Recommendation We remain Overweight on SG Property Developer sector. Our top picks within the property developer sector include Chip Eng Seng, CapitaLand and Banyan Tree.

|

Dehong covers primarily the REITs and property developer sector. He has close to 7 years experience in equities related dealing and research roles.

He graduated with a Masters of Science in Applied Finance from SMU and Bachelors of Accountancy from NTU.