The Positive

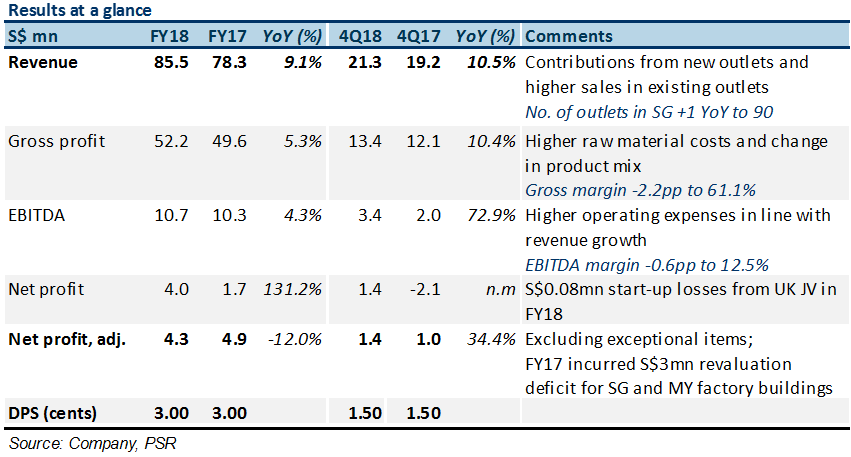

+ FY18 Revenue growth is the strongest in the past 5 years, mainly from underlying sales growth. Sales from retail outlets were up 9.2% YoY, driven by the +8.0% YoY average sales per store; and to a lesser extent, by the net one additional store count during FY18.

In addition, puff sales were up 3.3% YoY, and remained as the major revenue contributor (c.30% of the FY18 Revenue). We believe these figures are a testament to the Group’s successful product innovation.

+ 4Q18 Gross margin returned to c.63%; which should be sustainable. Gross margin has been depressed for the past 3 quarters. Average selling prices have been revised to pass on the higher raw material costs to consumers in Apr-18. It also benefit from a more favourable input prices arising from bulk purchasing, on the back of expanded factory space.

The Negative

– UK joint venture incurred S$0.08mn of start-up costs prior to opening. The Group is on-track to open its first flagship outlet in Covent Garden – London, United Kingdom in Jun-18.

Outlook

Positive outlook as growth momentum extend into FY19e. New stores opening and product innovations will continue to drive topline growth. The new factory will increase production capacity (in terms of variety and volume) to fuel their expansion strategy, and improve its margins via (a) enhanced manufacturing efficiencies and (b) cost savings from bulk purchasing.

Maintained Buy with unchanged DCF-derived TP of S$0.98

We have increased our FY19e sales growth expectation to 6.0% YoY from 4.1%. We also introduce FY20 estimates in his report. Core net profit is estimated grow by 21.6%/22.8% in FY19/20e as the Group continues to ramp up its product innovation effort while deriving better operating efficiencies from its new factory facilities and equipment.

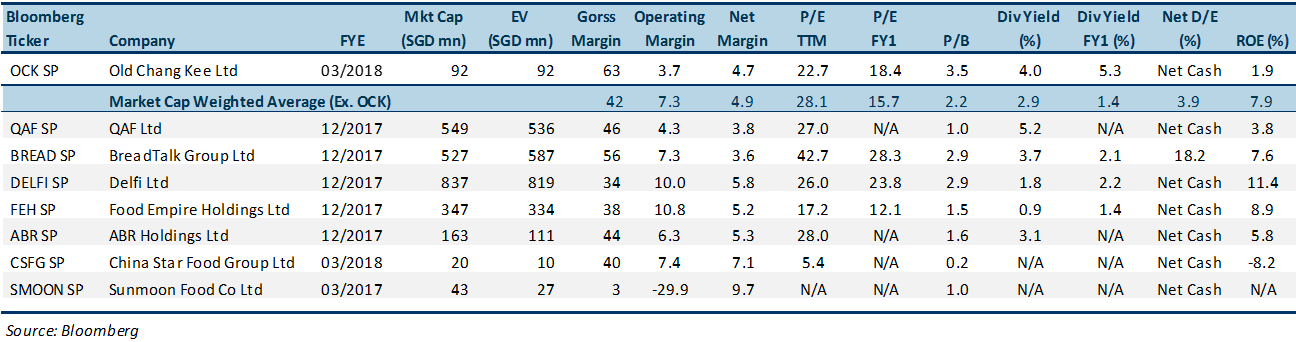

OCK is currently trading at 19% discount to its peers average of 28.1x. Our TP implies a F19e/FY20e PER of 22.6x and 18.5x, respectively.

We like the stock as we expect OCK to:

Figure 1: Comparables

Lin Sin has been an investment analyst in Phillip Securities Research since June 2014, where she started as an economist, focusing on China and ASEAN macroeconomics. Currently, she covers primarily the Consumers and Healthcare sectors in Singapore equities market.

She graduated with a Bachelor of Science in Mathematics and Economics from NTU.