The Positives

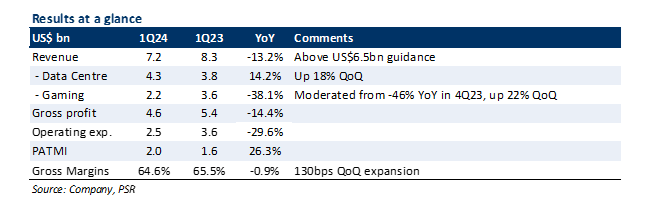

+ Revenue beat company guidance. Revenue was down 13% YoY to US$7.2bn, but this was above company guidance of US$6.5bn. The better-than-expected performance was driven by 14% YoY growth in Data Centre sales, which set a new record of US$4.3bn. NVDA attributed the growth to the surge in demand across its customer base (cloud service providers, consumer internet, and enterprises) who are looking to harness the technology of generative AI and large language models (LLMs) that use the company’s Hopper and Ampere GPUs.

+ Strong 2Q24 guidance. NVDA guided for a revenue of US$11bn (+/- 2%), which is ~53% above consensus estimates of US$7.2bn, and represents a 64% YoY growth, following YoY sales contraction since 3Q23. The company said the growth will largely be driven by its Data Centre business benefiting from the steep increase in demand related to Generative AI and LLMs. NVDA said this allowed it to extend its visibility of the segment’s business out a few quarters. Although no guidance was provided beyond 2Q24, NVDA noted that it will be procuring a significantly higher level of supply for 2H24, where it indicated that sales will be higher than that of 1H24. Gross margin is expected to be 68.6%, indicating a potential 25% YoY expansion (6.6% on a normalised basis as NVDA incurred a US$1.2bn inventory charge in 2Q23) as it sells more of its new H100 data centre GPUs, where we believe the price difference is as much as 200% compared to its previous A100.

The Negatives

– Gaming, Professional Visualisation contraction continues. Gaming/Professional Visualisation revenue declined 38%/53% YoY as both businesses continue to face macroeconomic headwinds and lower sell-in to normalise channel inventory. However, the contraction has moderated compared to 4Q23 where they declined 46%/65% YoY, and sales were up QoQ by 22%/31% as NVDA ramps its new GPUs based on Ada Lovelace architecture.

Maximilian mainly covers the US technology sector. In his strive to be a globalized citizen and get continuous exposure to the fundamentals of companies from various industries, he graduated from Singapore Management University holding a Bachelor’s degree in Business Management.