The Positives

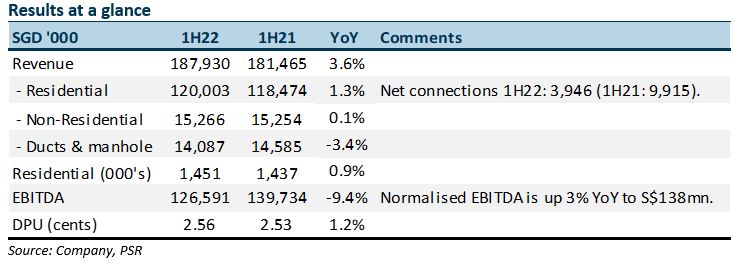

+ Normalised EBITDA expanded 3% YoY. Excluding the lease receivable remeasurement loss of S$12mn and grants and rebates last year of S$5.4mn, EBITDA is 1H22 would have risen 3.1% YoY to S$138mn (1H21: S$134.3mn). EBITDA growth came from the 38% revenue growth in diversion and co-location revenue to S$14mn. A rebound from last years circuit breaker disruption.

+ Lower interest expense. Finance cost was down 45% YoY to S$5.3mn. Borrowing cost has been lowered from 2.4% to 1.1% following the refinancing in June. Some of the hedges in the prior period has started to run off.

The Negatives

– Residential connections are still soft. New residential connections in 1H22 were only 3,946. A steep drop from 9,915 in 1H21. Our forecast for FY22e is lowered from 25,000 to 10,000 new connections.

Outlook

FY22e is a recovery from the circuit breaker disruption. Installation revenue from NBAP and diversion work rebounded from a low base last year. There is still a lingering impact from the pandemic due to delay in home construction, impacting residential connections. The increase in capital expenditure will depress dividends in the near term, but will build up the regulated asset base and yield returns in the next regulatory review

Our ACCUMULATE recommendation maintained on unchanged TP of S$1.03

NetLink’s dividend is stable with support from monthly recurring connection revenue and capital expenditure flexibility.

Paul has 20 years of experience as a fund manager and sell-side analyst. During his time as fund manager, he has managed multiple funds and mandates including capital guaranteed, dividend income, renewable energy, single country and regionally focused funds.

He graduated from Monash University and had completed both his Chartered Financial Analyst and Australian CPA programme.