Description

Microsoft Corporation develops, licenses and supports a range of software products, services and devices. The Company’s segments include Productivity and Business Processes, Intelligent Cloud and More Personal Computing. The Company’s products include operating systems; cross-device productivity applications; server applications, business solution applications; desktop and server management tools; software development tools; video games and training and certification of computer system integrators and developers. It also designs, manufactures, and sells devices, including personal computers (PCs), tablets, gaming and entertainment consoles, phones, other intelligent devices, and related accessories, that integrate with its cloud-based offerings. It offers an array of services, including cloud-based solutions that provide customers with software, services, platforms, and content, and it provides solution support and consulting services. It also delivers online advertising to a global audience.

Source: Thomson Reuters

Investment Rationale

MSFT reported their Q2 earnings on 31st January, with non-GAAP EPS of USD0.96, up 20% YoY, beating consensus estimates of USD0.86. However, due to President Trump’s Tax Cuts and Jobs Act, the company was required to report a GAAP EPS of a 0.82 loss, as GAAP did not allow the exclusion of extraordinary events. As such, the price of MSFT fell to about USD85.00 a share before reversing its downtrend to close at USD94.18 last night. MSFT’s earnings were actually better than expected, and registered impressive growth in key areas such as Cloud Computing (called Azure) revenue growth up 98% YoY. Given the continued growth in such key areas, we believe that despite the run up in MSFT’s price, there is further upside to be had in the future for the Company.

Recent Price Action: MSFT started its uptrend at the end of 2016, running up from USD60 to its last close of USD94.18. However, the market overreacted to the one off loss that the Company had to report after President Trump’s tax bill passed. Subsequently, the price recovered after that dip and is back to its price prior to the earnings release.

10th consecutive year of 90+% growth in Azure: Cloud Computing has been a great boon for many technology companies. Worldwide public cloud services industry revenue is expected to reach USD305.8bn in 2018, up from USD260.2bn in 2017.

Out of this lucrative market, MSFT has managed to carve out a large chunk of the market with its Azure offering. Amazon’s AWS is the market leader, but is ceding territory to MSFT. Azure reportedly climbed from 16% of the market share to 20% while AWS fell from 68% to 62%.

MSFT also reported that their Intelligent Cloud segment grew revenue to USD7.8bn, up 15% YoY. Azure itself grew revenue by 98%, marking the 10th consecutive quarter that Azure’s revenue has almost doubled. Azure revenue still amounts to only USD3.7bn out of MSFT’s reported USD28.9bn total revenue, and as such, we believe there is room for meaningful growth and contribution to MSFT’s earnings.

As such, given the expected continued growth of the sector, and MSFT’s dominant position and increasing market share, we believe there is still value to be had from this lucrative sector.

Office 365 continues to take off: Besides Azure, MSFT’s revamp of their legacy business with Office 365 has continued to boost their bottom line. The Company changed their traditional licensing business for Microsoft Office products to a cloud-base subscription model, and the change seems to have been good for them. Their Productivity and Business Process revenue was up 24% YoY to USD9bn, with Office 365 commercial revenue up 41% YoY. Towards the end of 2017, MSFT reported that Office 365 subscribers had outnumbered perpetual licenses and that they expected that by 2019, more than two-thirds of Office users would be 365 subscribers.

Microsoft Office remains an integral part of the commercial world and with the move to subscription-based model, MSFT secured a vital source of recurring revenue. With evidence that this source of revenue is continuing to increase, we are positive on MSFT’s ability to continue to grow both their top and bottom line.

Valuations: MSFT closed at USD94.18 and trades at a forward PER of 25.80, with a dividend yield of 1.73%. MSFT 4 year average PER is 24.80. MSFT’s total revenue for 2017 was USD98.86bn and over the past 5 years, it has been able to grow that revenue by about 5.70%. MSFT has been able to generate a free cash flow of USD31.38bn for FY17 and has been able to consistently grow their free cash flows, up from USD24.98bn in FY16 and USD23.72bn in FY15. MSFT currently pays an annualized dividend of USD1.68 per share, about 1.78% yield. It has a payout ratio of 46% and 14-year history of growing that dividend consecutively, one of the few technology companies that pay and grow their dividends. Given MSFT’s growth prospects, we believe that MSFT to be undervalued at current price.

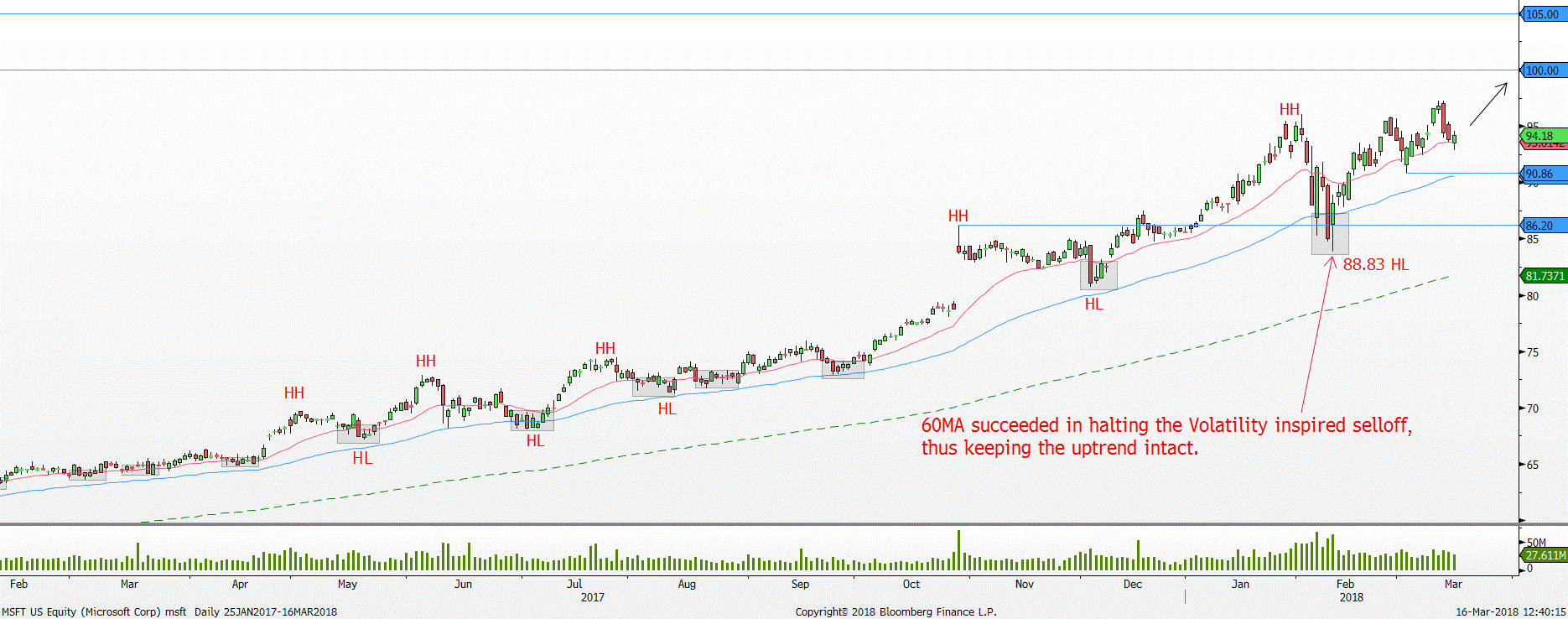

Technicals: MSFT has been moving in a stable uptrend since June 2016 with the 20 and 60-day moving average propelling price higher on every correction. The 20 and 60 day moving average is acting as a springboard each time MSFT goes into a correction selloff where the bullish momentum reengages shown by the highlighted areas.

MSFT Daily chart – Strong support from the 20 and 60 day moving average

Support 1: 90.86 Resistance 1: 100.00

Support 2: 86.20 Resistance 2: 105.00

Red line = 20 period moving average, blue line = 60 period moving average, Green line = 200 period moving average

Despite the recent Volatility spike incident in early February, the 60-day moving average managed to halt the selloff once again and return price into the uptrend. At one point, MSFT was down more than -12% from the 96.07 peak. Nonetheless, the strong bullish rejection off the 60-day moving average since 9 February 2018 has successfully resurrected the uptrend. Moreover, price kept the uptrend structure of the Higher Highs (HH) and Higher Lows (HL) intact.

Since then, price has stayed comfortably above both the 20 and 60 day moving average signals further sign of strength. For this current up-leg, buyers should be targeting the 100 psychological round number.

Moving forward, expect the 20 and 60-day moving average to continue providing a floor on price to halt and reverse the selloff.

Conclusion: We are bullish on MSFT due to 1) Cloud Computing and Azure, 2) Office 365 Subscriptions and 3) Valuations given MSFT’s growth prospects. As such, we believe that stock is undervalued and the recent recover signaling the continuation of its uptrend.