The Positives

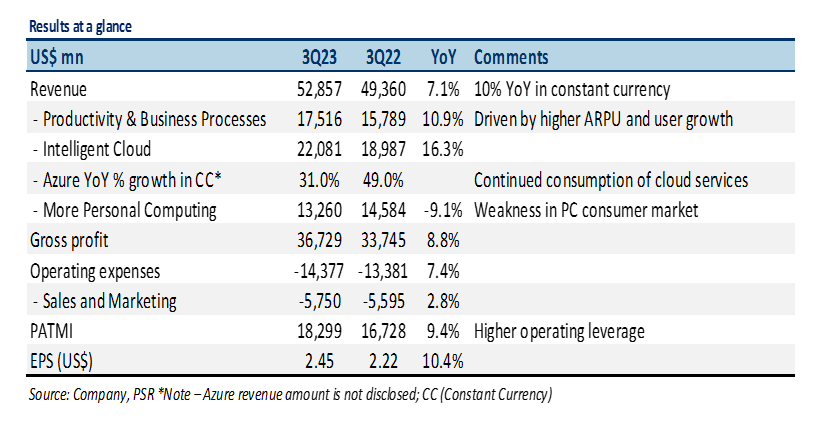

+ Azure remains the primary growth driver. In 3Q23, Azure cloud revenue grew by 31% YoY on a constant currency basis, in line with the company’s guidance. Growth continues to be driven by rising cloud adoption as enterprises look to lower operating expenses and digitize their operations. Management highlighted that Azure OpenAI Service customers spiked by 10x QoQ to more than 2,500 (Coursera, Grammarly, and Mercedes-Benz) indicating early traction for its next generation AI services.

+ Demand for Office 365 remains strong. Office 365 commercial revenue (under productivity and business processes) grew 18% YoY in constant currency driven by strong renewal trends and continued E5 momentum. Microsoft reported paid Office 365 commercial user growth of 11% YoY to 382mn led by small-to-medium business and frontline worker offerings. Management also highlighted that Teams surpassed 300mn monthly active users (vs. 280mn in 2Q23) with nearly 60% of Teams customers purchasing Teams Phone, Rooms or Premium.

The Negatives

– Deteriorating PC consumer market hurt Windows OEM revenue. Windows OEM revenue, which includes the sales of Windows software to PC makers, declined by 28% YoY. This is mainly due to weakening consumer demand for PCs, high inventory levels and macro economic uncertainty.