The Positives

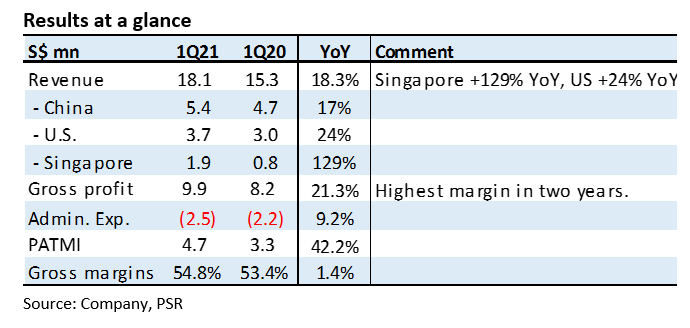

+ Record quarterly revenue of S$18.1mn. Revenue rose 18% YoY. Countries responsible were Singapore (+129%) and the U.S. (+24%). New projects from the U.S. as well as a resumption of work in the U.S. and Malaysia following lockdowns in the June quarter likely played a part.

+ Gross margins at a 2-year high. Following its lumpy capacity expansion in FY18, economies of scale have kicked in and revenue has increased to cover its additional fixed costs. New products also typically command higher margins.

+ Operating cash flow more than doubled. 1Q21 operating cash flow of S$7.1mn was more than double the S$3.2mn achieved a year ago. Net cash was S$25.5mn, up from S$19mn a year ago.

The Negative

– Spurt in capex. Capex spiked 4x YoY to S$2mn. MMH continues to guide for S$4-5mn for FY21. Capex front-loading might have been due to a surge in demand from customers.

Outlook

The cycle recovery remains nascent and growth this year should be further supported by new projects from its front-end semiconductor customer in the U.S. We believe the contribution could be almost 10% of revenue in FY21e.

Downgrade to ACCUMULATE, albeit with higher TP of S$2.93 (from S$2.50)

We are downgrading our recommendation from BUY to ACCUMULATE. Our FY21e earnings have been raised by 9% as we lift revenue by 5% to S$75.1mn. MMH provides attractive financial metrics, namely ROE of 33%, a net-cash position and a dividend yield of 4.9% remains attractive.

Paul has 20 years of experience as a fund manager and sell-side analyst. During his time as fund manager, he has managed multiple funds and mandates including capital guaranteed, dividend income, renewable energy, single country and regionally focused funds.

He graduated from Monash University and had completed both his Chartered Financial Analyst and Australian CPA programme.