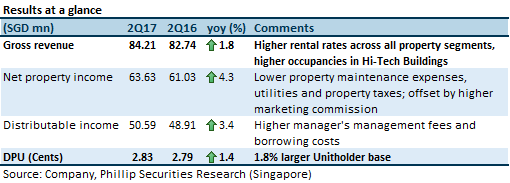

Occupancy remains healthy, but dips marginally; average passing rent maintained

Portfolio occupancy dipped marginally quarter-on-quarter (qoq) to 92.5% from 93.0%. Average portfolio passing rent was unchanged at S$1.92 psf/month. Lower qoq portfolio occupancy was due to Business Parks and Stack-Up/Ramp-Up segments. Rental reversions for the various segments ranged between -2.3% and +2.7%, with the weighted average of +0.7% for the portfolio (+0.5% in 1QFY17). Management shared that it would be a concern if portfolio occupancy falls below 90%; and it would have to recalibrate the existing leasing strategy.

Maintaining our cautious stance over FY18 lease expiry profile

Portfolio weighted average lease expiry (WALE) stands at 2.8 years. Management views the 6.8% of leases expiring in 2HFY17 “business as usual”. 32.8% of leases expiring in FY18 is a concern to us, as the current oversupply condition could persist until then, resulting in negative rental reversions and lower occupancy. Management did share however, that there are no concentrated leases expiring in FY18 that come to mind. Management thinks that the oversupply situation will improve in 2018, with the absorption of supply.

Organic growth strategies of BTS and AEI projects are on track

Phase one of the Hewlett-Packard build-to-suit (BTS) project had obtained its Temporary Occupation Permit (TOP) on October 21. Management expects rental contribution to commence on December 1. Phase Two should be completed in another six months.

Construction works at the Kallang Basin 4 Cluster asset enhancement initiative (AEI) project had commenced in August 2016. The project is on track to be completed in 1Q CY2018. Management shared that the property remains 0% pre-committed, and would expect better clarity only six months prior to completion of the project.

Strong balance sheet favourable for inorganic growth

Gearing remains low at 29.0% and there is firepower to make acquisitions. Management remains open to acquiring outside of Singapore. Management did highlight that data centres are a possible segment, as there is strong demand for the asset class.

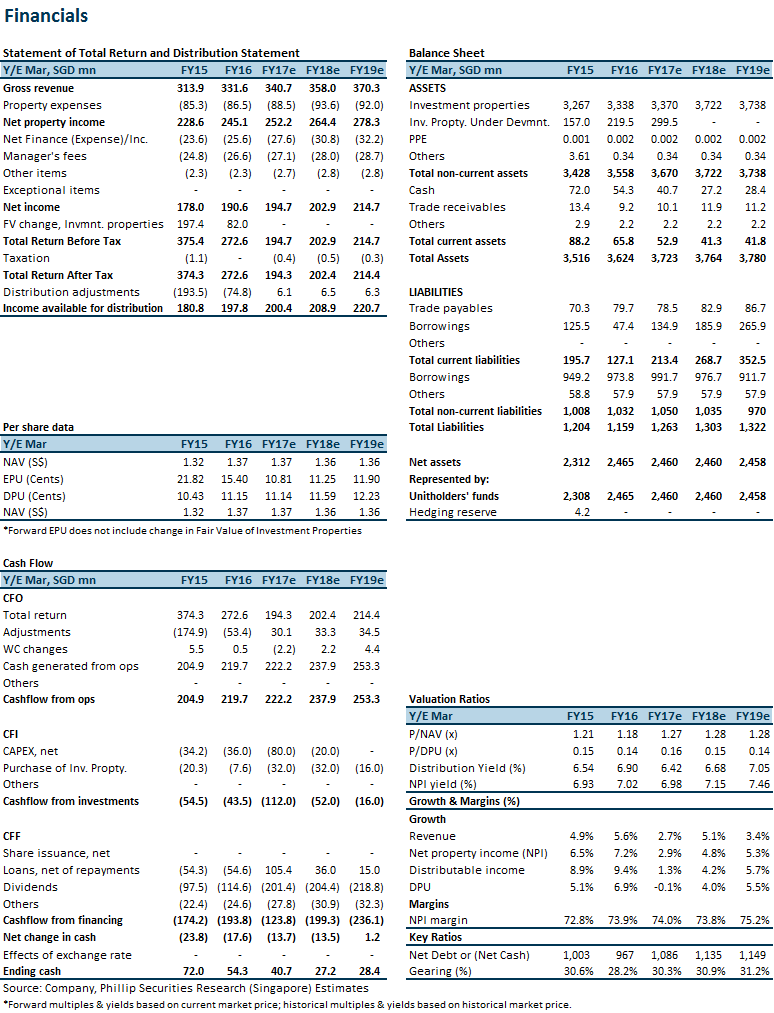

Maintain “Neutral” rating with unchanged DDM valuation of S$1.74 (pervious: S$1.72)

Our forecasts remain largely intact and fair value is marginally higher. We are expecting some short-term pain with lower qoq DPU over the next three quarters, due to the rent free-period for the Hewlett-Packard BTS being spread across 18 months.

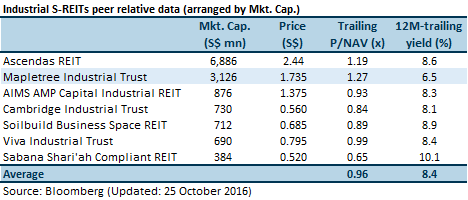

Peer relative valuation

MINT is trading above the sector average P/NAV multiple and lower than the peer average 12M-trailing yield.

Richard covers the Transport Sector and Industrial REITs. He graduated with a Master of Science in Applied Finance from the Singapore Management University. He holds the CFTe and FRM certifications and is a CFA charterholder.

He was ranked #2 Top Stock Picker (Asia) for Real Estate Investment Trusts in the 2018 Thomson Reuters Analyst Awards, and ranked #2 Top Stock Picker (Singapore) for Resources & Infrastructure in the 2016 Thomson Reuters Analyst Awards.