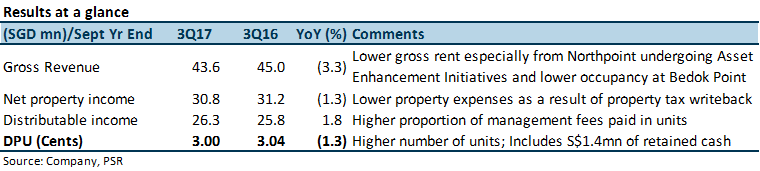

The positives

+ Causeway Point (CWP) continues to support earnings: Contributing 53% of portfolio net property income (NPI), CWP was one of only two malls with positive YoY growth in NPI for 3Q17 (+5% vs portfolio -1.3%). Occupancy cost remains low (c.16.5%) at the mall despite a drop in tenant sales. (FCT FY16: 15.7%, CMT FY16: 19%).

+ Northpoint (NP) 90% pre-committed 2months from completion: Enhancement works is expected to complete on schedule in September 2017. Management guided that they are on track to achieve the targeted 9% increase in gross rents post-AEI, or even better.

+ Expo Downtown Line 3 to open 21 October 2017, adjacent Changi City Point (CCP) expected to see better occupancies: Occupancy at the mall has improved from 81.1% at FY16 to 87.4% as at 1 July 2017. As the new station opens, we expect CCP to recover from the 80+% occupancy rates it has suffered due to the construction works.

The negatives

– Suburban malls’ rentals continue to drop as evident from slowing reversions: 3Q17 portfolio rental reversions at 0.4%, the weakest level for the year (1Q: 6.9%, 2Q: 4.1%).

– Higher portfolio shopper traffic (+3.7% YoY) at malls did not translate to higher tenant sales: Tenant sales remain weak (-3.3% YoY excl. NP), although this is an improvement from the prior 3-month period (-6.9% YoY excl. NP).

Outlook

We expect retail sales and spot rents to recover by 2H17 and 1H18 respectively, though the recovery will be weak. With Northpoint and Changi City Point looking to perform better by year end post-AEI, and the opening of DTL3, the improved occupancies at these malls should support DPU. Together with CWP, these three malls contributed c.85% of NPI in 3Q17. DPU is expected to remain stable despite the improved operating performance as management reverts to taking lesser fees in units (leaving less cash for distribution).

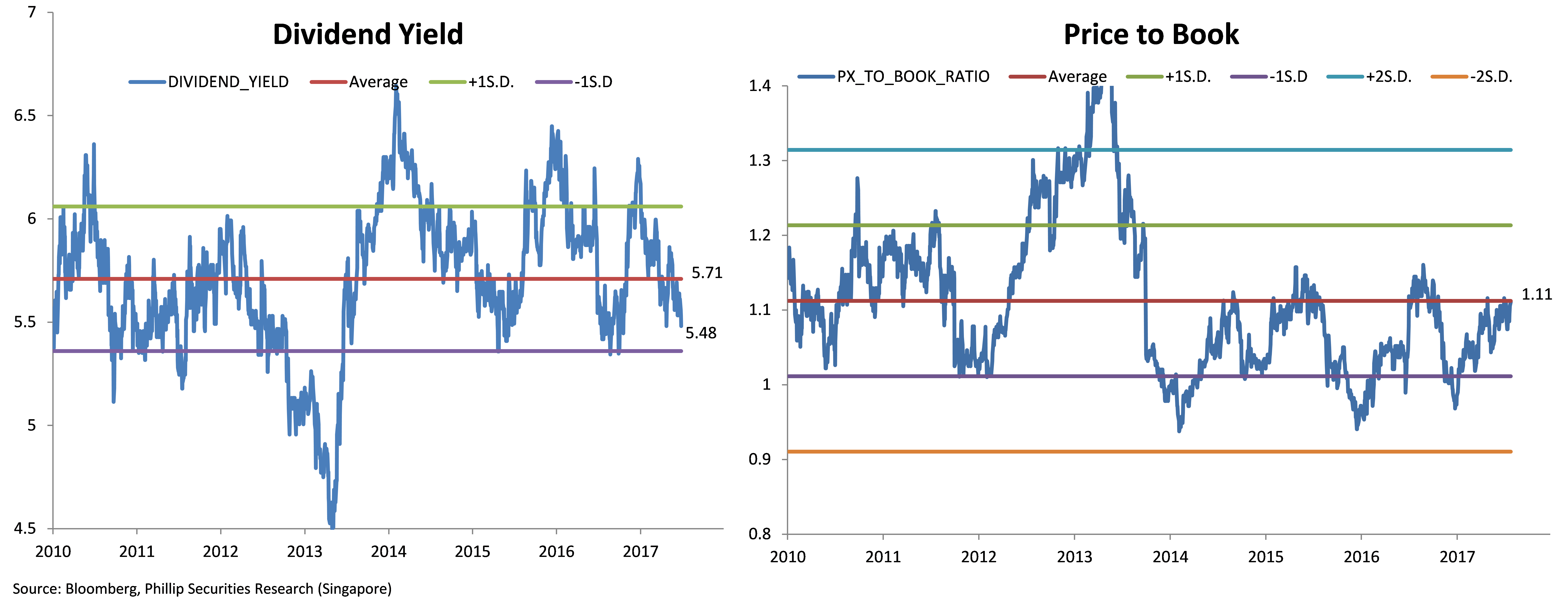

Maintain NEUTRAL with a higher target price of S$2.14.

We raised our FY18e/FY19e DPU by 3.8%/4.7% to reflect the better operating performance of post-AEI-Northpoint and Changi City Point. Accordingly, our target price increases from S$2.04 to S$2.14. This translates to an FY17e yield of 5.6% and P/NAV of 1.11.

Figures 1 and 2: FCT trades at below post-GFC average yield and close to average P/NAV

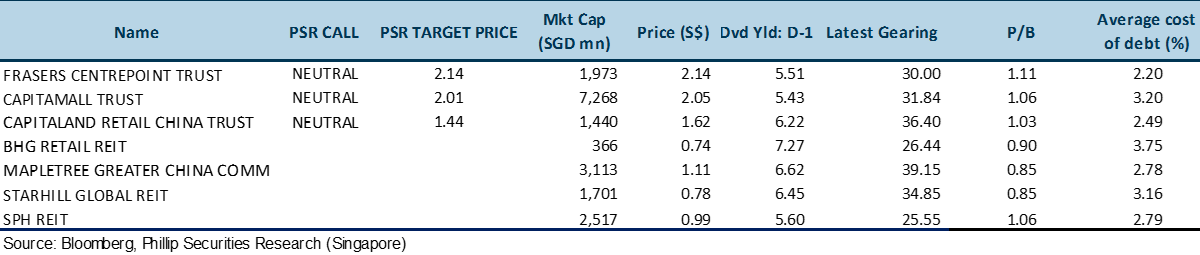

Figure 3: Peer comparison table

Dehong covers primarily the REITs and property developer sector. He has close to 7 years experience in equities related dealing and research roles.

He graduated with a Masters of Science in Applied Finance from SMU and Bachelors of Accountancy from NTU.