The Positives

+ All-in interest costs largely stable. Average all-in cost of financing stands at c.4% as of end Dec 2017, largely unchanged from the preceding year.

+ Rebound in portfolio valuation after drop in FY16. Portfolio valuations grew 1.7% in FY17 (excluding acquisitions in same year). This comes after a drop of 1.2% in the preceding year. Valuer’s forecasted cashflows likely improved after the uptick in Singapore CPI numbers for 2017.

The Negatives

– Total Receivables grew 78% to S$53mn from S$29.8mn in FY16. This was mainly due to delay in advance rental receivables from tenants.

Outlook

The outlook for organic growth in FY18 is positive after the uptick in Singapore CPI for 2017 (0.6% for Jan-Nov) vs -0.5% in 2016. Rental escalations for FIRT’s Indonesian hospitals are determined by Singapore CPI numbers for the preceding year. This is however slightly lower than our forecasted CPI of 1% for 2017. We adjust our forecasted overall rental escalations for FY18 from 2% to 1.5%. Acquisition pipeline from sponsor’s network of 40 hospitals remain stable with earmarked acquisition targets for FY18.

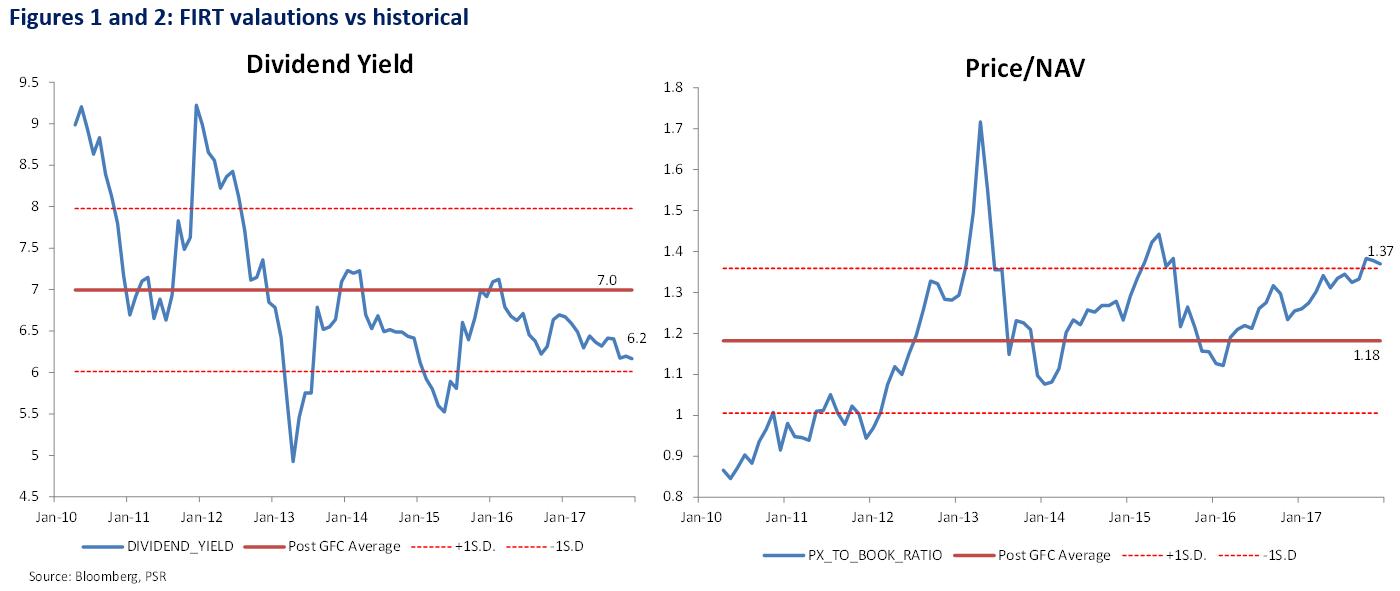

Maintain NEUTRAL with unchanged target price due to rich valuation

FIRT currently trades at the upper range of their average valuation boundaries (figures 1 and 2) since post GFC. As we roll forward our forecasts to FY18, we lower our terminal growth rate from 1% to 0.5% to account for the higher drop-off in valuations from BOT (leasehold) properties. We maintain our NEUTRAL rating with unchanged target price of S$1.32. Our target price translates to an FY18e yield of 6.5% and P/NAV of 1.27.

Dehong covers primarily the REITs and property developer sector. He has close to 7 years experience in equities related dealing and research roles.

He graduated with a Masters of Science in Applied Finance from SMU and Bachelors of Accountancy from NTU.