The Positive

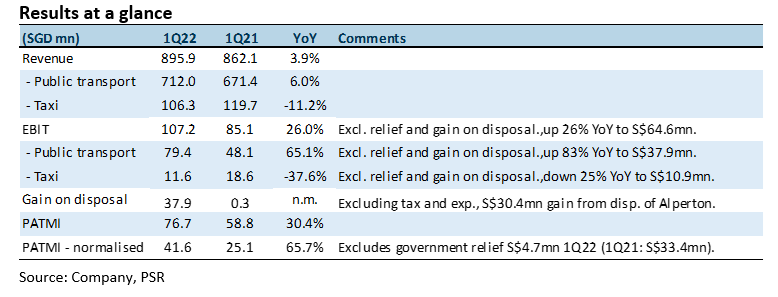

+ Improvement in public transport. Rail volumes were down 4% YoY in 1Q22. Revenue recovered due to fuel indexation and bus chartering business. Revenue rose $40mn YoY, of which $17mn, or 42%, flowed to operating earnings. Operating margins jumped from 3% in 1Q21 to 5.3% in 1Q22.

The Negative

– Taxi still weak. Taxi revenues fell 11% YoY due to the 7% drop in the Singapore taxi fleet, divestment of the London taxi business and continuation of taxi rental rebates, especially in China. Despite the decline in fleet size, we believe taxis currently have a competitive edge over private hire vehicles due to a higher percentage of hybrid vehicles and lower fuel costs of 15-20%.

Outlook

The 15% rebate on taxi rental will continue until September 2022. However, effective 1 May, CD will impose a 4% booking fee on drivers that use its CDC Zig app. Assuming $200 of daily bookings per taxi, the additional S$8 revenue can offset the estimated S$15 to $18. At risk will be taxi operations in China. The pandemic lockdown especially in Beijing will require the need for rental waivers for taxi drivers. Public transport services (or rail) should benefit from workers returning to the office in Singapore. Upcoming CAPEX commitments include EV buses, EV taxis and EV charging stations.

Maintain BUY with unchanged TP of S$1.80

We find ComfortDelgro attractive for the expected 5% dividend yield, net cash balance sheet of S$578mn and share price still 40% below pre-pandemic levels.

Paul has 20 years of experience as a fund manager and sell-side analyst. During his time as fund manager, he has managed multiple funds and mandates including capital guaranteed, dividend income, renewable energy, single country and regionally focused funds.

He graduated from Monash University and had completed both his Chartered Financial Analyst and Australian CPA programme.