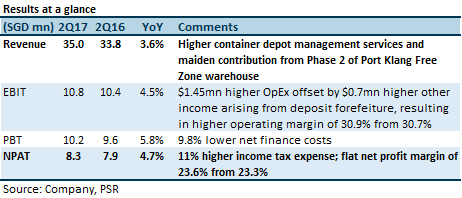

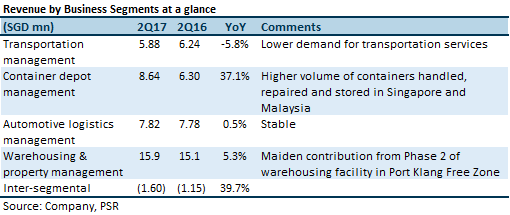

The positives

The negatives

Outlook

The outlook is positive. While there is a warehouse oversupply situation, we see additional earnings coming from the container repair, maintenance and washing JV, which began operations in July. At the same time, the contribution from the Jurong Island Container Depot (JICD) project is not meaningful yet. Further out, we are expecting the JICLF project to drive more than 40% earnings growth in FY19e when it becomes operational. Risk to our view comes mainly from the final completion date of JICLF.

Maintain Buy; slightly lower target price of S$1.12 (previously $1.18)

Some minor adjustments to our forecasts, and FY17e dividend assumption. Following the unusually high interim dividend declared, we now assume no final dividend will be proposed in FY17. We also have a higher WACC of 7.6% (previously: 7.4%). Our target price represents an implied 16.5x FY17e P/E multiple, compared to the Straits Times Index next-twelve-months P/E multiple of 14.7x.

Richard covers the Transport Sector and Industrial REITs. He graduated with a Master of Science in Applied Finance from the Singapore Management University. He holds the CFTe and FRM certifications and is a CFA charterholder.

He was ranked #2 Top Stock Picker (Asia) for Real Estate Investment Trusts in the 2018 Thomson Reuters Analyst Awards, and ranked #2 Top Stock Picker (Singapore) for Resources & Infrastructure in the 2016 Thomson Reuters Analyst Awards.