Positives

+ Carbon-in-leach (CIL) plant is under construction: The group has been working on the CIL project since 1Q17 and expects to complete construction in mid Nov-17. Preliminary estimation of newly-added capacity will be 150k to 180k tonnes of ore processed. CIL will enhance efficiency in extracting gold with maximum 30 ppt increase in recovery rate from the current average 65% at the existing heap leaching facilities. At the moment, the group is speeding up the construction progress, inasmuch as it has located spots with higher ore grade, from which it specifically plans to extract gold by harnessing CIL. It is expected to have one and a half months of trial production in FY17.

+ Ongoing exploration for Pulai and KelGold project: For the Pulai project, the group completed 3 drill holes in 2Q17, but the results failed to meet Geology Department’s expectation. Based on the previous magnetic survey showing some anomalies, the group decided to conduct diamond drilling with 11 designed drill holes in the potential iron deposit area in 3Q17. For the KelGold project, soil sampling program has been carried out since May-17 and will last till Aug-17. As of Jun-17, 2,560 samples were collected and 48.24km of designed tracks were surveyed.

Negatives

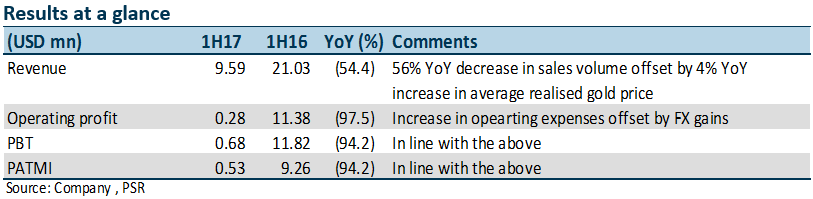

– Low ore grade dragged the performance: The total sales volume of gold only arrived at 3,670 oz in 1H17, compared to 17,079 oz in 1H16. The dive was attributed to substantial fall in ore grade. Though average realised selling price (ASP) increased to US$1,277/oz during the period (1H16: US$1,231/oz), the group delivered an unsatisfactory performance.

Outlook

We believe the low-grade situation could continue to late FY17 until the trial run of CIL plant. Hence, the FY17 performance is expected to be the worst since 2012. The short-term catalyst that could be looked forward to is the possible turnaround by incorporating CIL’s results in FY18. From a long-term perspective, it is expected to create synergies from monetising on minerals from Pulai and KelGold.

Investment action

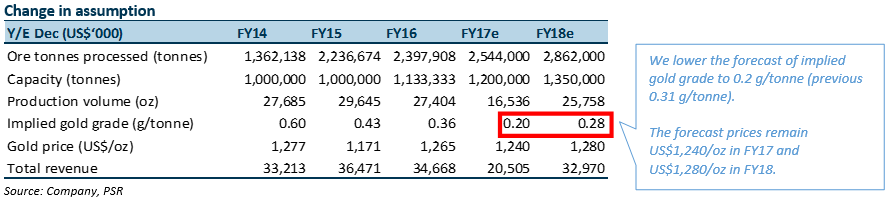

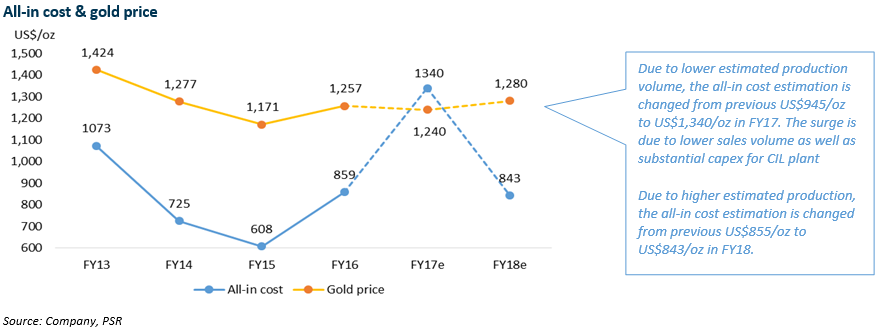

1HFY17 output has been a disappointment. We cut our earnings forecast by 84.6% for FY17e but raise earning forecast by 17.7% for FY18e respectively. Similarly, we lower our TP to S$0.29 (previous: S$0.44), and we downgrade our recommendation from BUY to NEUTRAL. We are upbeat on gold prices and expect the current lacklustre production to recover in FY18.

Guangzhi graduated from Singapore Management University with a Master degree in Applied Finance and from South China University of Technology with a Bachelor degree in Electronic Commerce.

The current sector coverages include Energy, Utilities, and Mining sectors. He has 3 years experience in equity research in both Hong Kong and Singapore market. He is the mandarin spokesperson for Phillip Securities Research in relation to China-related projects and all mandarin seminars and client events.