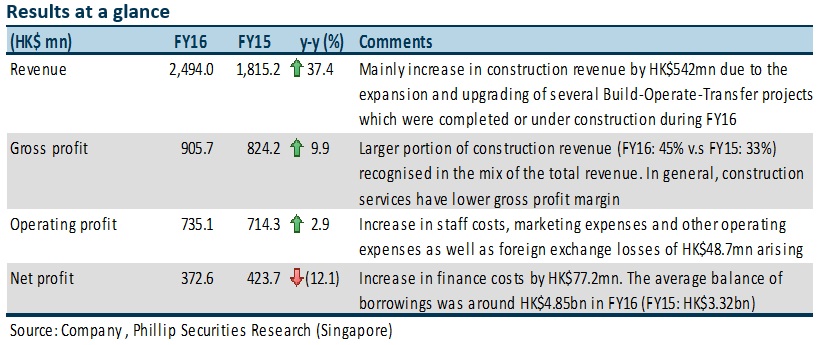

The revenue mix is c.45% construction revenue to c.34% operation revenue in FY16, as compared to FY15’s c.33% Construction Revenue to c.42% Operation Revenue. Management guided the gross profit margin (GPM) of construction segment is c.20% while that of operation segment ranges from 50% to 60%. Moving forward, CEWL will continue to focus on project upgrades and accelerate Sponge city construction. In terms of update on Sponge city, currently CEWL has completed over 30% of progress with more than 40 projects under operation simultaneously. CEWL targets to complete the Sponge city by early 2018. Since construction remains the main revenue contributor for CEWL, we expect GPM could decline further as the share from construction services increases.

CEWL’s major financing channels are through bank loans, which increased the Group’s interest burden. Management guided that long-term loans will predominate shares in borrowings. Moving forward, CEWL expects to accomplish panda bond issuance in FY17. Furthermore, once the acquisition of projects, especially integrated one like Sponge city, scales up, demanding huge expenditure that is much larger than the cost of current projects, the group would consider to establish a water fund that involves other parties’ funding. Throughout this, CEWL is able to reserve liquidity amid expansion.

Though both CEWL and local government have not reached any solutions that repaying receivables to the Group by cash and other assets, government had started to pay back receivables in 4Q16. Since the central government never relaxes the regulation on water treatment standard, management is confident that this issue will be settled as negotiation continues.

The management guided that there are 4 beneficial trends that support the Group’s positive outlook.

Investment Action

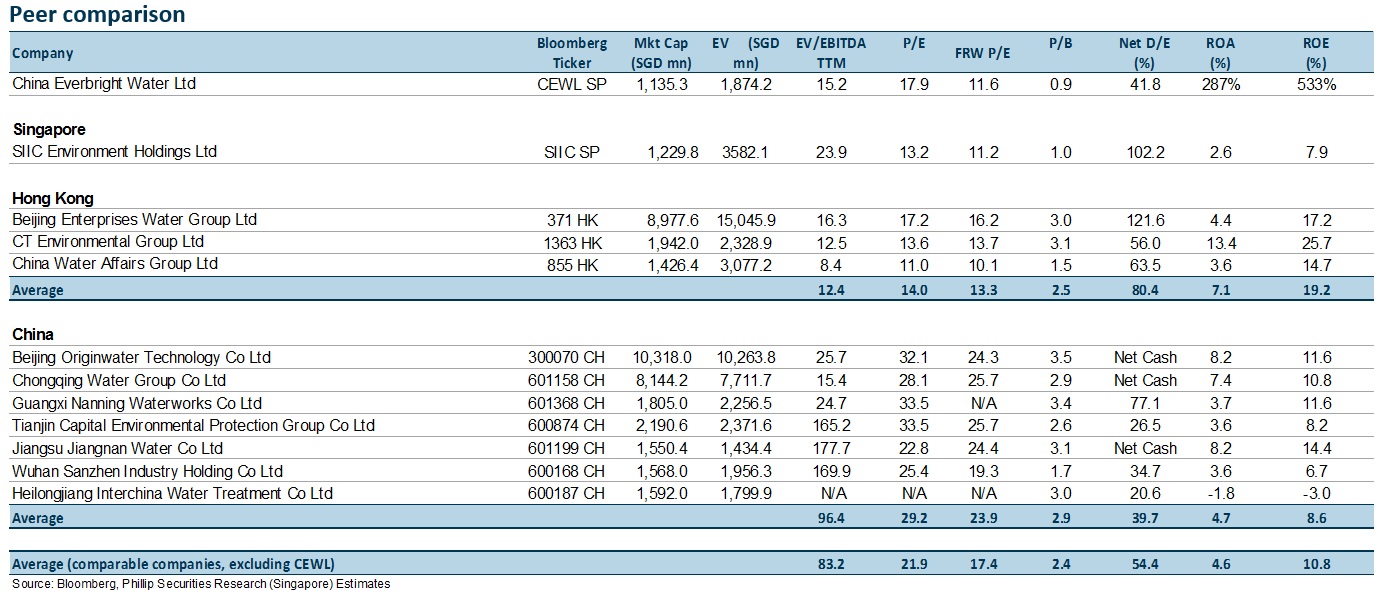

We maintained our FY17 EPS forecast of 3.2 SG cents, and upgrade our call to “Buy” with a reduced TP of S$0.56 (previous SG$0.63), based on lower average forward PER of 17.4x (previous 19.8x), together with forecast 0.4 SG cents dividend, implying a potential return of 29.8% from closing price.

Guangzhi graduated from Singapore Management University with a Master degree in Applied Finance and from South China University of Technology with a Bachelor degree in Electronic Commerce.

The current sector coverages include Energy, Utilities, and Mining sectors. He has 3 years experience in equity research in both Hong Kong and Singapore market. He is the mandarin spokesperson for Phillip Securities Research in relation to China-related projects and all mandarin seminars and client events.