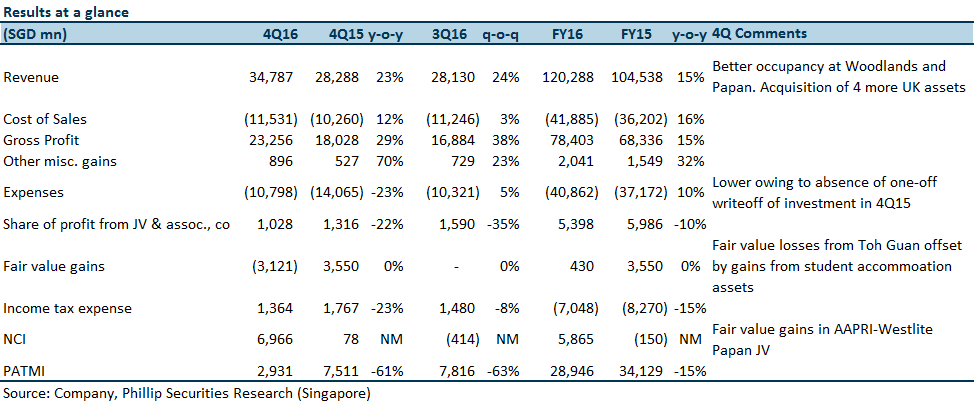

The growth was contributed by four new student accommodation properties in United Kingdom acquired in 3Q16 and by improved occupancy for workers’ dormitories at Westlite Woodlands (90% in 4Q16 vs. 75% in 3Q16) and ASPRI-Westlite Papan (75% in 4Q16 vs. 20% in 3Q16). Positive rental reversions of approximately 3% from Australian and United Kingdom student accommodation business also supported the revenue growth. We expect the renovations and upgrades to student accommodation assets in the United Kingdom and Singapore to support a c.3% rental growth in FY17F.

Management estimates that a progressive reduction in supply of Temporary Purpose-Built Worker Accommodation (“PBWA”) and Factory Converted Dormitories (“FCD”) over time would cause a total shortage of between c.150,000 and c.180,000 PBWA beds. Management expects the stricter conditions for FCDs that came into effect from 1 January 2017 would force some FCDs out of the market and cause more foreign workers to shift into PBWAs. At the same time, an estimated net decline of 6,000 PBWA beds owing to expiration of c.35,000 temporary PBWA beds in 2017 would weigh down on available supply. As the shortage gap widens this year, we expect occupancy for Westlite Dormitories to ramp up quickly to hit full capacity by end of 2017.

Currently the URA Master Plan zoning type for the Westlite Tuas is “Business 2” which provisions an ancillary component for workers’ dormitory use. The renewal of the lease and its conditions are still under negotiations. However, we continue to assume that the lease will not be renewed and have excluded earnings projection for Westlite Tuas after 1Q17.

The Westlite Bukit Minyak project has broken ground and it is expected to be completed in 2018. Thus we revised our projections and expect Westlite Bukit Minyak to begin operations in mid-2018 (previously beginning of 2019).

Plans for a new accommodation block has been finalised but the additional capacity has not been disclosed. We do not expect the AEI to disrupt the existing occupancy.

Downgrade to “Accumulate” from previous “Buy” rating with an unchanged price of SGD0.420. Recent price movement met our expectations based on our assumptions of Centurion Corporation Limited’s operations. But further upside can be expected if the land lease on Westlite Tuas is renewed subject to the terms of the renewal.

Jeremy covers primarily the Banking and Finance sector. He has 6 years’ experience in equities related dealing and research roles.

He graduated with Bachelors of Mechanical Engineering from Nanyang Technological University.