+ Portfolio value remains stable with slight tightening of capitalisation rate. Same store valuation of 126 properties was stable at S$9.84b vs. S$9.75bn a year ago. (Total AUM of S$10.35bn.) Portfolio capitalisation rate compressed slightly from 6.29% to 6.24%. This was driven by tightening of the weighted average capitalisation rate of the Singapore portfolio by 5bps, and tightening of the Australia portfolio by 10bps.

+ Portfolio value remains stable with slight tightening of capitalisation rate. Same store valuation of 126 properties was stable at S$9.84b vs. S$9.75bn a year ago. (Total AUM of S$10.35bn.) Portfolio capitalisation rate compressed slightly from 6.29% to 6.24%. This was driven by tightening of the weighted average capitalisation rate of the Singapore portfolio by 5bps, and tightening of the Australia portfolio by 10bps.

+ Occupancy remained stable with net positive rental reversions. Total portfolio occupancy was higher QoQ from 91.1% to 91.5%. Both Singapore and Australia portfolio exhibited the same stability in occupancy. Total portfolio achieved +0.7% rental reversion for FY17/18, but -6.8% reversion for 4Q FY17/18.

+ Healthy balance sheet at 34.4% aggregate leverage. Aggregate leverage is marginally lower QoQ from 35.2%. Ample debt headroom of ~S$1bn (to 40% leverage), potentially growing the AUM by ~10%. Average debt maturity has improved from 2.8 years to 3.2 years. Debt maturity profile is staggered, with a policy of no more than 20% of total debt maturing in any given year.

Outlook

The outlook is stable. The portfolio is sufficiently diversified to cushion any short-term localised impact. The manager guided for a soft leasing market this year, but possibility of positive rental reversions coming from Business Park and Hi-Specs properties. Overhang of supply will continue to put pressure on logistics assets.

The manager also shared on its acquisition/growth strategy. Singapore will remain the key market for the portfolio, with overseas assets making up 30%-40%. Apart from looking for opportunities in the existing overseas market of Australia (specifically the eastern seaboard), the manager is actively looking at other new markets. The manager favours Europe and US as they have similar risk profiles to where the REIT already has exposure to. Entry into new markets will be on a platform basis, with key criteria of being scalable and having long-term benefit to the REIT.

Maintain Accumulate; higher target price of $2.91 (previously $2.89)

Our forecast remains largely unchanged. We expect a stable ~6% yield and our target price gives an implied 1.37 times FY18/19e forward P/NAV multiple.

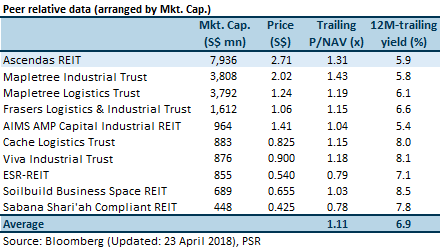

Relative valuation

A-REIT is trading above the peer average P/NAV multiple and at a lower 12M-trailing yield than the peer average.

Richard covers the Transport Sector and Industrial REITs. He graduated with a Master of Science in Applied Finance from the Singapore Management University. He holds the CFTe and FRM certifications and is a CFA charterholder.

He was ranked #2 Top Stock Picker (Asia) for Real Estate Investment Trusts in the 2018 Thomson Reuters Analyst Awards, and ranked #2 Top Stock Picker (Singapore) for Resources & Infrastructure in the 2016 Thomson Reuters Analyst Awards.