The Positives

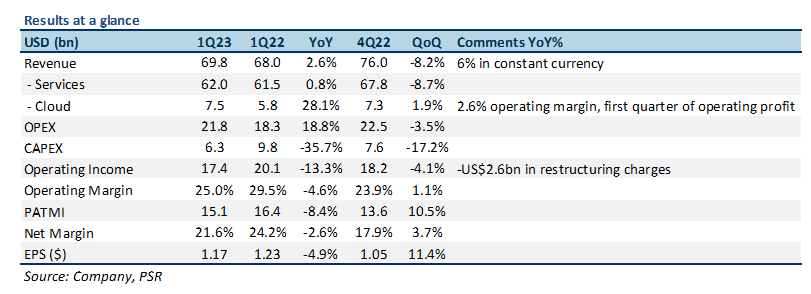

+ Revenue growth re-accelerated slightly due to advertising revenue. GOOGL saw a re-acceleration in revenue growth, posting total revenue of US$69.8bn, 3% YoY (4Q22: 1%). Growth was driven by a 2% YoY increase in advertising revenue from Search (4Q22: -2% YoY) as spending from its travel and retail verticals improved. Additionally, ad revenue from YouTube showed some signs of stabilisation, declining only 3% YoY (4Q22: -8% YoY) as YouTube Shorts monetization increased, offset by some incremental pullback in advertiser spend.

+ Google Cloud momentum slowing, but turned the corner on profitability. Cloud saw some slowdown in its growth momentum, with revenues up 28% YoY (4Q22: 32% YoY). This was led by a continued weaker macro environment, with customers choosing to optimise their current Cloud consumption instead of expanding. Even with topline growth slowing, Cloud posted its first profitable segment, with operating income of US$191mn (1Q22: US$706mn) – operating margin of 2.6%, as management remained focused on driving longer-term profitability in this segment.

+ Earnings in-line with our forecasts. GOOGL announced 1Q23 PATMI of US$15.1bn, in line with our expectations as the company continued to be more prudent with expenses. Earnings were hurt by a US$2.6bn one-off restructuring related charge, offset positively by a US$1bn reduction in depreciation expenses due to an increase in estimated useful life of servers and other equipment, and a delay in timing of its stock-based compensation. 1Q23 PATMI was at 21% of our FY23e forecasts, with Adj. PATMI (excl. restructuring charges) at 24% of our forecasts.

The Negative

– Cautious FY23e outlook. Given the ongoing uncertainty in the macro environment, management remained cautious for the remainder of FY23e, expecting advertising revenue growth to remain muted, with continued decline in Cloud momentum.

Jonathan covers the US technology sector focusing on internet companies. Formerly a national and professional athlete, he graduated from the University of Oregon with a Bachelor’s Degree in Social Sciences.