Positives

+ Increased takeaway and delivery sales. 1H21 net profit was 35% higher HoH as increased takeaway and delivery sales mitigated the lower footfall during Singapore’s move into Phase 2 (Heightened Alert) from 16 May to 13 June. Both Dough Culture and R&B Tea were the most resilient due to the nature of its business, and saw increased takeaways and delivery sales.

+ Footfalls improved in Macau, outlook positive. Macau reopened its borders to foreigners via mainland China on 16 March 2021. This led to a slight improvement in footfalls at its malls and food courts during the recent Labour Day holidays in May 2021. All of Koufu’s food courts at the University of Macau, Nova City and Cotai Sands remained operational, though footfall and revenue were about 39% lower than pre-COVID levels. The negative impact was cushioned by rental waivers and rebates from landlords.

+ TOP obtained for integrated facility, operations to begin progressively from 3Q21. The group has obtained TOP in April 2021 for its integrated facility, which is expected to commence operations progressively in the second half of the year. It will be occupying 75% of the total gross floor area with the balance 25% tenanted out. We expect cost synergies from the move to the integrated facility.

+ New outlets secured. The group has secured a food court at Outram Community Hospital and a R&B tea kiosk at Sinopec Petrol Station in Woodlands Ave 5 which is scheduled for opening in 3Q21. It will also be opening a Dough Culture kiosk at Jurong East MRT station and a Grove quick service restaurant at Northshore Plaza to be opened in 4Q21. We expect these to contribute positively to the Group’s revenue stream when they come onboard.

Negatives

– Footfall at 65% of pre-Covid levels. Despite a lifting of dining-in prohibitions at all food outlets, footfall at its outlets has been hurt by the limit of two persons for social gatherings, reduced capacity for malls and work from home as the default mode. Koufu’s food court and Grove quick service restaurant at Singapore Management University and three R&B Tea kiosks at Singapore Management University, Far East Square and Change Alley Mall remain suspended due to low footfalls at these outlets.

Outlook

As Singapore moves into endemic Covid-19, we see a more positive outlook. We expect more measures to be lifted in a calibrated manner, including a further relaxation of limits on dining in. Work from home may also no longer be the default arrangement. We expect improved footfall at Koufu’s outlets as a result.

We also expect cost synergies from FY22e as its supply chain and logistics will be strengthened together with a broadening and expansion of its production capabilities at its new integrated facility. This is expected to lead to higher productivity and product margins. We raise FY22e PATMI by 1% to account for some of these cost-savings. In addition, there will be rental income from the tenancy of nine stalls in a coffee shop, 24 cloud kitchens and 132 beds in the staff dormitory at the integrated facility.

In terms of expansion plans, the group has opened one new food court with one self-operated F&B stall at Sun Plaza, two new R&B tea kiosks at Fusionpolis and Sun Plaza, three Dough Culture kiosks at Sing Post Centre, Sun Plaza and Oasis Terrace in 1H 2021. The Group has further opened 2 new food courts at Marina Square, Nanyang Technological University and 1 new food court shop at the new Koufu Headquarters in Q3 2021. It has also lined up a few new outlets to be progressively opened in 3Q21 and 4Q21.

Macau’s footfall has also improved with an easing of border restrictions. We expect business to improve as more mainland Chinese visit the country under quarantine-free travel arrangements. These are only granted to the most low-risk areas of China at the moment.

Maintain NEUTRAL with unchanged TP of S$0.64

We maintain our NEUTRAL rating and TP of S$0.64, still based on 18.5x FY21e P/E. We remain cautious on the re-opening roadmap due to a resurgence of Covid-19 in Singapore and China. The stock could potentially be re-rated if there is further relaxation of dine-in measures and an increase in foreign travellers to Singapore.

Positives

+ Marked improvement in footfalls in Singapore and Macau. 2H20 footfalls at outlets and malls recovered slightly as the economy reopened. We estimate that food courts located near offices recovered by 30% HoH in 2H20 as restrictions eased. Footfalls and demand in food courts and coffee shops in the heartlands were stable. Footfalls in Macau recovered by 30% in 2H20 even though this was still about 60% below pre-COVID levels.

+ Marked recovery for F&B Retail in 2H20. F&B Retail was its biggest drag in 1H20 as this segment does not have fixed rental income from stall tenants, unlike Outlet & Mall Management. A resumption of operations after the circuit breaker in this segment led to an uptick in takings. Revenue in 2H20 was up 43% HoH. The uplift was also helped by contributions from Deli Asia Group, acquired on 30 July 2020.

+ New store openings resumed in 2H20; more to come in 2021. The Group opened one new food court, two R&B Tea kiosks and two Dough Culture kiosks in 2H20. The two new Dough Culture kiosks brought total outlets to nine since its acquisition of Deli Asia Group last year. The Group now expects to hit its target of 20 Dough Culture kiosks in three years instead of five under its previous plan.

For 2021, the Group has secured and will open three new food courts at Sun Plaza, Woodlands Height (Koufu’s new HQ) and NTU in the second quarter of 2021.

Koufu opened a third food court in Macau at Nova City in 3Q20. The current occupancy for food stalls remains at 100% even though business operations remain at reduced levels (~40% pre COVID-19) given lower number of visitors and travellers. Mainland China and Macau have slowly reopened its borders, along with the lifting of the 14-day quarantine policy on the Macau-Guangdong borders in July 2020.

Negatives

– Consumption recovery slower than expected. With work from home being the default arrangement, consumption recovery at food courts near offices, downtown and in tertiary institutions remains slow. Footfalls at Rasapura Masters and Elemen Restaurant at Marina Bay Sands remain low as travel restrictions are still in place. We estimate that footfalls and takings at both will remain at 45% of pre-COVID-We19 levels this year.

– Expected TOP of IF delayed again, to 1Q21. The progress of the construction of the IF has been delayed due to the COVID-19 measures introduced in both Singapore and Malaysia (where certain materials have been sourced from). The Group expects further delay in the TOP, to be in the first quarter of 2021, at the earliest, as the commencement of construction has been delayed. Management now expect to move into the IF in the second quarter of 2021 and to commence operation in the second quarter of 2021. The Group will be occupying 75% of the total gross floor area while the balance of 25% has been full tenanted out.

In light of the slower than expected consumption recovery, we lowered our revenue estimates for FY21e and FY22e by 6.5% and 6.2% respectively. Consequently, profit for FY21e and FY22e is reduced by 11.5% and 10.4% respectively from negative operating leverage and the delay in completion of the IF.

Update on Deli Asia acquisition

Koufu completed its acquisition of Deli Asia on 30 July 2020. The acquisition is expected to fast-track its revenue diversification and expansion to complementary dim-sum snacks, fried foods and dough products. Deli Asia will give it access to new markets such as the supply of frozen and partial fried food products to third-party businesses, including supermarkets and overseas markets.

Since its acquisition, two new kiosks have been opened, in 2H20. Another three are in the pipeline this year. Management now expects to hit its target of 20 Dough Culture kiosks in three years instead of five. We expect Deli Asia to contribute about S$2.7mn and S$3.2mn in profits in FY21e and FY22e respectively.

Cost-savings expected from move into integrated facility. The Group will move the manufacturing of Deli Asia’s food products to its new integrated facility when ready. This will save it rental costs from the two facilities that Deli Asia currently operates in.

Outlook

We continue to remain positive on the Group’s outlook post circuit breaker. We believe the recovery in consumption post circuit breaker will continue to improve footfalls and revenue of the food courts and coffee shops in 2021. We expect the completion of the Group’s new IF in 1Q21 to yield cost savings and provide an additional revenue source from the rental of the balance 25% space. Koufu has proposed a final dividend of 0.7 cents per share for 2H20, bringing FY20’s payout ratio to 67% of earnings. The Group is currently in the midst of sourcing for buyers for their two existing central kitchens, we see the announcement of a sale of their existing central kitchens as a catalyst for the Group.

Positives

+ Marked improvement in footfall in Phase 2 of Singapore’s reopening after the circuit breaker. We estimate that Outlets & Mall management saw a 20% fall in footfall in the heartland areas during the circuit breaker period. Footfalls and revenue of the food courts and coffee shops located in the heartlands have seen significant improvements – to about 90% pre-COVID-19 levels - after the resumption of dine-in services. Business operations in Macau have also resumed operations albeit at significantly lower footfall.

+ F&B retail that saw the greatest hit in 1H20 sees marked recovery. The F&B retail segment was the biggest drag on 1H20 revenue from as it does not have fixed rental income from stall tenants like the Outlet & Mall management segment. The temporary suspension of 10 food courts, 3 quick-service restaurants (QSR), 2 full-service restaurants and 26 R&B tea kiosks/QSR during the circuit breaker and Phase 1 periods have also reopened and have seen a significant uptick in takings after the circuit breaker.

+ New store openings resumed. The Group secured and opened two new coffeeshops and one R&B Tea kiosk in 1H20. They also opened their first R&B Tea kiosk in Indonesia on 4 July 2020. The opening of one new food court at Le Quest, Bukit Batok initially slated for opening has been delayed to the fourth quarter of 2020. The Group expects to open one quick service restaurant at Canberra Plaza and three new R&B Tea kiosks at Fusionpolis, Change Alley Mall and Le Quest in 2H20. The opening of one new food court at Nova City in Macau is also slated for opening in 3Q20.

Negatives

– Expected TOP of Integrated Facility (IF) pushed to 4Q20, at the earliest. The progress of the construction of the IF has been delayed due to the COVID-19 measures introduced in both Singapore and Malaysia (where certain materials have been sourced from). The Group expects further delay in the TOP to be in the fourth quarter of 2020, at the earliest, as the commencement of construction has been delayed. On a positive note, management informed that construction has resumed and they expect to move into the IF in the first quarter of 2021. In light of this new development, we have revised downwards our earnings estimate for FY21e and FY22e by 3.2% and 2.9% respectively.

– Footfalls at food courts located near offices, down-town areas, tertiary institutions as well as tourist hot-spots continue to remain low. With the resumption of most of the operations, footfalls at food courts located near offices, down-town areas, tertiary institutions as well as their Rasapura Masters and Elemen Restaurant at Marina Bay Sands continue to see low footfall which is expected to persist in 2H20.

Update on Deli Asia acquisition

Koufu has completed the acquisition of Deli Asia on 30 July 2020. The acquisition of Deli Asia is expected to fast-track Koufu’s revenue diversification and network expansion in complementary dim sum snacks, fried food and dough products. The acquisition will allow them to gain access to new markets through the supply of frozen and partial fried food products to third party businesses, including supermarkets and exports to overseas markets. According to management, they have plans to further expand their network of seven retail outlets under Dough Culture brand to 20 in the next five years.

Cost savings expected from move into IF. They also expect to move the manufacturing of Deli Asia’s food products to the new IF, which will allow them to benefit from rental savings from the two facilities that Deli Asia is currently operating in.

Outlook

We continue to remain positive on the Group’s outlook post circuit breaker. We believe the recovery in consumption post circuit breaker will continue to improve footfalls and revenue of the food courts and coffee shops in 2H20. We expect the completion of the Group’s new IF in 4Q20 to see cost savings and an additional revenue source for them. Koufu has announced a dividend of 0.5 cents per share against 1H20 earnings per share of 0.46 cents, signaling their confidence in the 2H20 recovery.

Maintain BUY with lower TP of S$0.77 (previously S$0.80)

We are maintaining our BUY rating with a lower TP of S$0.77. We tweak our FY21e and FY22e earnings estimates down slightly by 3.2% and 2.9% respectively as the TOP of the Group’s IF gets delayed to 4Q20 from 3Q20 previously.

Company Background

Koufu is a household name in Singapore, well known for its chain of food courts and coffee shops under management. Koufu has expanded rapidly over the years and now operates a multitude of brands island-wide. As at end 2019, the Group operates 50 food courts (including 2 in Macau), 16 coffeeshops, 76 F&B retail stalls (including 4 in Macau), and 26 R&B Tea and Supertea in Singapore.

Investment Merits

Outlook

We are positive on the outlook. We see the recovery in consumption post circuit breaker will be a huge positive for the Group. The new IF is expected to be operational from 3Q20, which will see cost savings and additional revenue. For 3Q20, Koufu is also expected to open two new food courts and two new R&B tea kiosks.

Initiating coverage with a BUY rating and target price of $0.800

We initiate coverage on Koufu Group with a BUY recommendation and a target price of $0.80. We peg Koufu to a PE of 18.5x FY21e, which is the sector average. We view Koufu as best in class with a defensive business model and superior growth profile from their overseas expansion plans and the expansion of their new concepts (R&B Tea and their premium vegetarian Elemen restaurants). We like their historical record of generating positive free cash flow and forecast the Group to generate strong free cash flow of S$25m a year from FY20e to FY22e. Their strong balance sheet (FY19 net cash of S$86m or S$0.15 per share) puts them in good stead to ride out the current crisis as well as to take advantage of M&A activities to grow.

Background

Koufu is an established Singapore household name well known for its chain of food courts and coffee shops under management. From just two food courts and one coffee shop in 2002, Koufu has expanded quickly over the years and now operates a multitude of brands island-wide. As at end 2019, the Group operates 50 food courts (including 2 in Macau), 16 coffeeshops, 76 F&B retail stalls (including 4 in Macau), and 26 R&B Tea and Supertea in Singapore.

In July 2018, Koufu’s IPO on the Mainboard of the SGX raised net proceeds of S$43 million set aside for the development of an integrated facility with it’s expected completion in 3Q20.

The Group focuses on different market segments with different price ranges (see Figure 3), and are able to grow their customer base, expand their market share and capture different customers in each of the market segment they serve through different offerings.

We are positive on the Group’s expansion in the mass-market segment – with a price range between S$20 to S$50 - as this segment has seen the highest growth. From 2008 – 2018, the F&B food service sector grew by a CAGR of 2.4% according to Singstat and is expected to continue growing by 2% going forward. The recent economic slowdown in our view will fuel more consumers to switch from the high-end market segment to the mass-market segment, benefitting mass-market operators such as Koufu.

Investment Merits

The new IF is expected to better support all of their F&B retail business and cater to future business expansion, thereby creating new and recurring revenue streams for the Group. An example of this is by allowing Koufu to leverage on their platform to partner F&B operators and lease spaces on-demand, to help small F&B establishments minimise food preparation areas at their existing outlets and stalls.

Initiating coverage with a BUY rating and target price of $0.800.

We initiate coverage on Koufu Group with a BUY recommendation and a target price of $0.800. We peg Koufu to a PE of 18.5x FY21e, which is the sector average. We view Koufu as best in class with a defensive business model and superior growth profile due to their overseas expansion plans and the expansion of new concepts (like R&B tea and their premium vegetarian restaurant concept Elemen). We like their historical record of generating positive free cash flow and forecast the Group to generate strong free cash flow of S$25m a year from FY20e to FY22e. Their strong balance sheet (FY19 net cash of S$86m or S$0.15 per share) puts them in good stead to ride out the current crisis as well as to take advantage of M&A activities to grow.

Industry

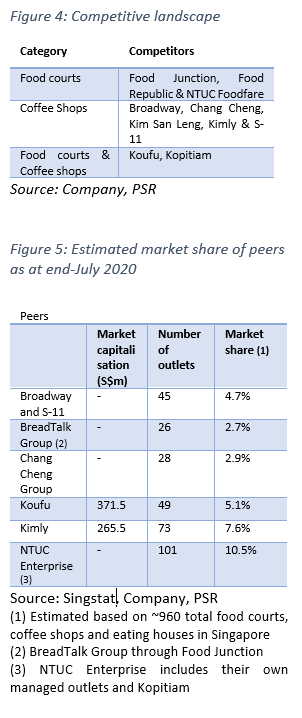

The F&B industry (including the operation and management of F&B outlets) in Singapore is very competitive. Aside from other indirect F&B competitors, in the area of operation and management of food courts and/or coffee shops, there are a number of large chain operators, and we have categorised these into the different categories in Figure 4.

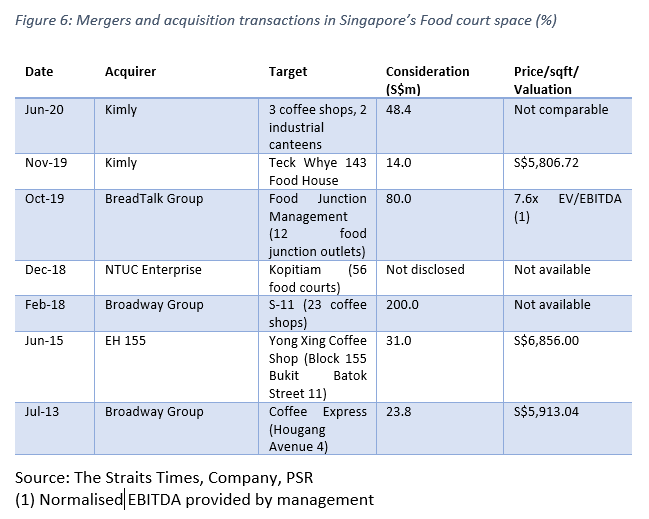

Based on statistics from Singapore’s Department of Statistics in 2015, there are a total of 960 food courts, coffee shops and eating houses in Singapore, which generated approximately S$1.29 billion in operating receipts. Without the availability of public information on the rest of their peers, we made estimates on the market share of some of the biggest players in Singapore based on what is publicly available. We estimate that the top three players own less than 25% of the market share today. This presents considerable potential to expand and acquire a larger market share in the coffee shop and food court industry, and we have already seen this happening.

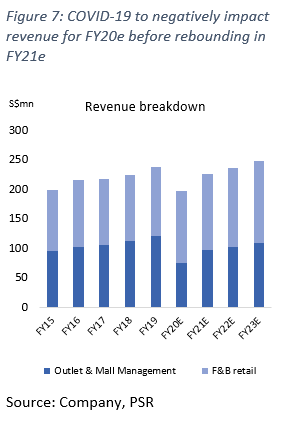

We think the desire to achieve greater economies of scale will drive F&B players to continue their expansion plans organically and through acquisitions. This industry consolidation has already seen the different players increase their market share in the market in the last three years. We have provided a summary of some of the major mergers and acquisitions that have taken place in the Singapore food courts space in the last few years below in Figure 6.

Moving forward, we think the pace of food court consolidation could accelerate as the major players aim to grow inorganically. This could mean greater competitive pressures for all the industry players. Nonetheless, we think there remains room to grow, and view the growth of food court operators here positively as they continue to achieve greater economies of scale and cost savings from their expansion.

Revenue

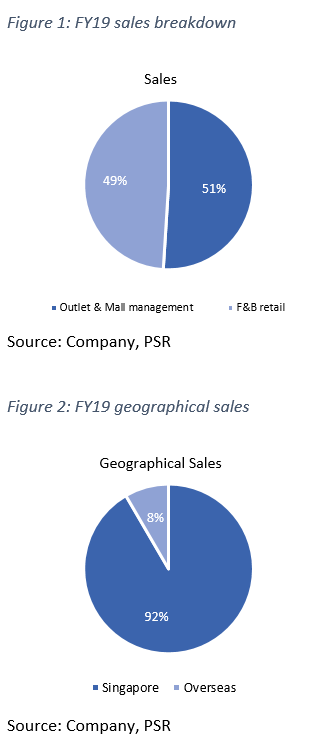

Outlet & mall management comprises 51% of FY19 revenue. Koufu operates and manages food courts and coffee shops in Singapore and Macau, as well as a hawker centre and a commercial mall in Singapore. Similar to a master tenant, Koufu sub-divides the gross floor area of the space, and charges rent and other auxiliary fees to their tenants. They also have self-operated F&B stalls offering drinks, fruits, desserts and dim sum within their food courts and coffee shops.

They operate their food courts and coffee shops under different revenue models. Most of the stall operators of their food courts are charged the higher of a fixed monthly fee or variable monthly fee (which we estimate to be in the range of around 18 – 22%) pegged to gross turnover of the F&B stall, which is dependent on the location of the food court, the mix of stall operators at that particular food court or the type of F&B products sold by the stall operators.

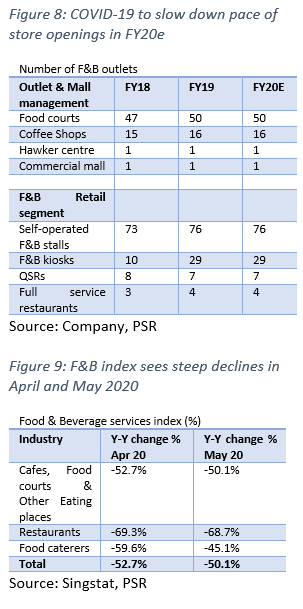

We think Outlet & mall management will take the biggest hit from COVID-19 in 2QFY20e and forecast this segment to decline by 30.8% for FY20e. Koufu has been able to consistently grow the revenue of their outlet & mall management over the years (Figure 7), led by increased stall openings, steady improvement in same-store sales growth (SSSG) and expansion overseas. We expect the closure of borders on the 23 March and the circuit breaker on the 7 April this year however to affect the overall footfall in their food courts and hawker centres which should see the steepest fall amongst their other offerings. We think Koufu’s Rasapura Masters food court at Marina Bay Sands (MBS) is the most negatively impacted by the restrictions on overseas visitors while their Elemen restaurants have been hit by dine-in restrictions and work from home arrangements. That said, we think the impact on food courts located in the heartlands will be less impacted by COVID-19 as consumers can still order takeaway at these outlets.

F&B retail comprises 49% of FY19 revenue. Koufu sells a variety of food and beverages in their self-operated F&B stalls, F&B kiosks, QSRs and full-service restaurants under their F&B retail business segment. Their self-operated F&B stalls are located within their food courts and coffee shops in Singapore and Macau. They operate the drinks stall in all the food courts and coffee shops operated by them. Their drinks stalls sell a variety of beverages including those that are made upon order, such as coffee, tea and other self-made, bottled and canned drinks. In addition to the sale of beverages, they also sell beer products and cigarette products at the drinks stalls of certain food courts and coffee shops. They usually also sell a mixture of fruits, desserts and dim sum at each food court or coffee shop.

Koufu also operates F&B stalls which offer a variety of F&B products across different cuisines, some of which are sold under our 1983 A Taste of Nanyang, The Western Plate, Hungry Jack and Hock Kee Hainanese Chicken Rice brands, in their food courts and coffee shops.

We expect the pace of stall expansion in the F&B retail segment to slow down this year as the reduced footfall and traffic is expected to negatively impact sales for the year. That said, the majority of Koufu’s outlets are located in the heartland areas, which should mitigate the fall in traffic due to the circuit breaker measures as compared to some of their peers with predominant presence in commercial malls.

Overall, we expect Koufu’s FY20e revenue to see a 18.4% y-y decline vs. FY19 (excluding the acquisition of Deli Asia) before rebounding higher by 14.3% in FY21e driven by the overall consumption recovery and new store openings as the authorities continue to reopen the economy and relax travel restrictions in both Singapore and Macau.

Expenses

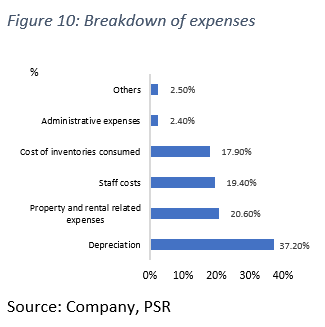

The Group leases substantially all of their premises for their F&B outlet in Singapore and Macau. Most of their existing leases have tenures of between three and four years at inception. They generally commence renewal negotiations with a landlord about six months before the expiry of each lease. Following the adoption of Singapore Financial Reporting Standards (SFRS (I) 16 Leases in 2019, Depreciation and Property and related expenses now form the bulk of their overall expenses at 57.8% (see Figure 10).

The Group’s IF at Woodlands Avenue 12 (Figure 11) is expected to result in cost savings for the Group through improved productivity and operational efficiency. The Group plans to move into a bigger central kitchen once the IF attains the temporary occupation permit (TOP) in 3QFY20e, which was delayed from May 2020 due to COVID-19, and we expect the IF to be operational by FY21e. The IF has 7-stories with a GFA of 20,000 sqm, more than five times larger than their current central kitchens and headquarters. The IF has a 30 years lease period from 2018. The new central kitchen will expand the Group’s central procurement, preparation, processing and distribution functions and the Group intends to lease out up to 30% of the total GFA to their stallholder to better support their F&B outlets and self-operated F&B stalls. The central kitchen might also be used to supply food products to third parties, providing an additional source of revenue for the Group.

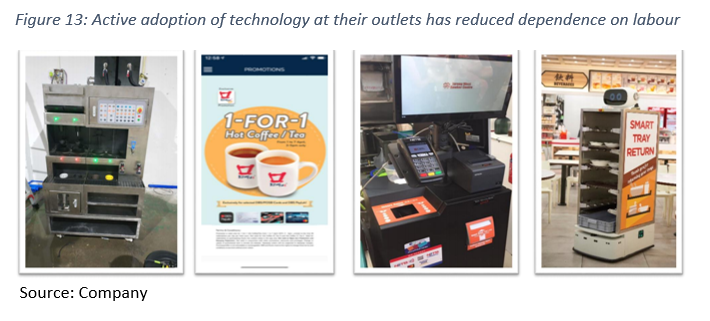

Koufu has actively adopted the use of technology to improve overall productivity and continues to embark on various projects to improve productivity through innovation. In particular, the traditional coffee making machine started its first pilot outlet at Blk 289 Compassvale Crescent in July last year, and the 2nd generation machine is set to be tested. The Group also started the mobile ordering application, which has been implemented at 41 food courts and coffee shops. This is to encourage self-ordering and payment collection. They have also increased the number of smart tray return robots to 43 currently deployed to 16 food courts and coffee shops.

Cash Flow

Koufu has a demonstrable track record of generating positive free cash flow. Koufu operates a highly cash-generative business with a negative cash conversion cycle of 24 – 40 days. F&B transactions are conducted on a cash basis while the Group usually negotiates credit terms of between 30 to 60 days with their suppliers. For that reason, the Group can consistently generate positive free cash flow (FCF) in its operating history. We expect the Group to see FCF dip in FY20e due to COVID-19 and the outlay for the IF which, is set to be completed by 3Q20. We expect the Group’s FCF to rebound strongly from FY21e as capital expenditure related to the IF will be fully fulfilled by then.

While Koufu has no fixed dividend policy in place, it has paid out dividends of 2.2 and 2.5 Singapore cents for FY18 and FY19 respectively, representing 46 – 50% dividend payout ratio. Given the Group’s strong cash-generating ability and net cash position, we think the Group is likely to maintain a 50% payout ratio for FY20e – FY23e, translating into a dividend yield of 2.0% - 3.8% over FY20e – FY23e.

We see the possibility of a possible special dividend upon the completion of their IF in 3Q20, which could see the sale of the two central kitchens in which they currently operate in at 18 and 20 Woodlands Terrace (one for non-Halal food preparation and another for Halal food preparation). Based on guidance from management, the sale of the two central kitchens will likely result in a S$8 million gain for the Company (1.4 Singapore cents per share) to be distributed to shareholders (or an additional 2.1% dividend yield), we have not imputed this gain to our financial projections given the uncertainty as to when this will take place.

Balance Sheet

Since their listing, Koufu has maintained a net cash position, with net cash of S$86 million (as at latest FY19) or S$0.15 per share. In our view it allows them to take advantage of synergistic M&A opportunities that come along the way (like we highlighted under the Industry consolidation), and to weather the ongoing COVID-19 crisis.

Despite the sharp decline in foot fall across the island due to the COVID-19 circuit breaker, we expect Koufu’s operations to remain relatively resilient due to the proximity of their food courts in the heartland areas which should help mitigate the overall fall in F&B sales. We also expect the Job Support Scheme and rental relief to help reduce overall costs faced by the Company. We provided the following estimates in Figure 15 to illustrate the amount of grants Koufu can be expected to have based on their total workforce mix and entitlement. The rental support from their landlords, which we estimate to be around three months on a blended basis will also help to mitigate their property rental expenses for FY20e, though this is also dragged down by the three months fixed rental waiver that is passed on to their tenants.

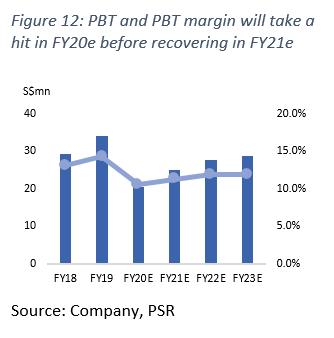

We expect Koufu to remain profitable in FY20e but with profit for the year down 38.8% on a y-y basis vs. FY19, excluding the contributions from their latest acquisition of Deli Asia, more on this later. We, therefore, expect Koufu to remain in a net cash position through FY20e – FY23e as the local authorities continue to open the economy and consumption resume.

Superior returns profile vs. SGX-listed peers

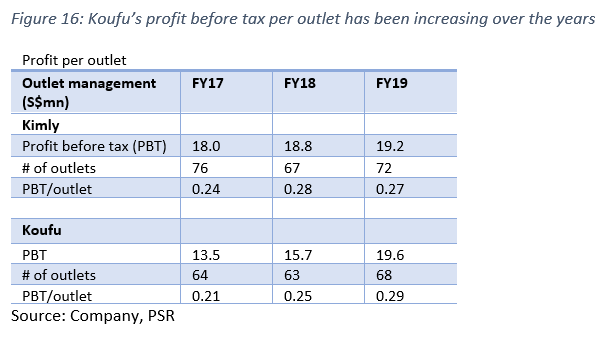

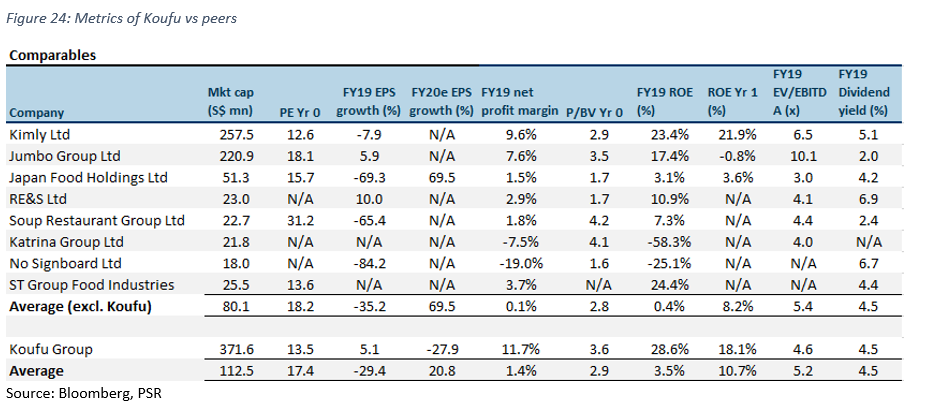

We view Koufu as best in class with a superior return profile vis-à-vis their peers. Their net margin of 11.7% in FY19 far exceed the sector average of 0.1% (excluding Koufu) (it is 2.8% when we remove outliers from our calculation). We also estimate that their profit before tax for the Outlet & Mall management segment has been growing over the years, and is the highest in FY19.

Their strong earnings profile also means that Koufu’s ROE is the highest amongst their SGX-listed peer group, with ROE for FY19 at 28.6% vs. their peer average of 0.4% (it is 14.4% when we remove outliers from our calculation). We believe the recent economic slowdown will fuel more consumers to switch from the high-end market segment to the mass-market segment, benefitting mass-market operators such as Koufu. In addition, we expect the Group’s expansion into overseas markets and the expansion of new concepts (such as R&B Tea and their Elemen restaurant) to act as future growth engines for them.

Expansion plans

Koufu furthers expansion in Macau and other ASEAN countries. Since opening their first overseas Koufu food court at Sands Cotai Central in 2012, the Group has been actively expanding its presence in Macau with a third food court targeted to open in 2Q20 now moved to 3Q20 due to the impact of COVID-19. Koufu has introduced “1983 – A Taste of Nanyang” and “Supertea” brands into Macau and has also made headway into new and vast markets – Malacca, Malaysia and Jakarta, Indonesia. Moving forward, we think the Group will leverage on their experience in Singapore and Macau to enter into China, Thailand and Australia.

Expansion of Elemen full-service restaurants into China, Malaysia, Indonesia, Thailand and Australia. We think the Group will look to expand Elemen into China, Malaysia, Indonesia, Thailand and Australia. As for the tea beverage brands, Koufu has already expanded into the neighbouring region, with the “R&B Tea” and “Supertea” brands. In Indonesia, they have formed a joint venture to bring tea beverages to Jakarta’s grade A malls. In Melaka (Malaysia), Koufu has secured a lease to open its first “R&B Tea” outlet in November 2019. Going forward, we think they will look to expand into the Philippines and Thailand through joint ventures, though this will likely be delayed at this stage amid the ongoing COVID-19 outbreak.

At home, Koufu is expanding its outlets in the mass-market segment through the opening of new foodcourts and F&B outlets. We are positive on the Group’s expansion in the mass-market segment – with a price range between S$20 to S$50. This segment is the fastest growing category. From 2008 – 2018, the F&B food service sector grew by a CAGR of 2.4% according to Singstat. We expect growth to sustain at least by 2% going forward. The recent economic slowdown in our view, will fuel more consumers to trade down from the high-end market segment to the mass-market segment, benefitting operators such as Koufu.

Given the current economic climate, we think Koufu will proceed more cautiously with store openings for FY20e and FY21e, and have baked this into our assumptions. That said, the Group continues to expand its store count for the year. In terms of new stores opening, Koufu opened one new R&B tea kiosk (Eastpoint Mall) and two coffee shops (Blk 602 Tampines Avenue 9 and Blk 215C Compassvale Drive) in the first quarter of 2020. For the rest of 2020, the opening of two new food courts and two new R&B tea kiosks initially slated for opening in the second quarter of 2020 has been moved back to the third quarter of 2020 tentatively.

Acquisition of Deli Asia earnings accretive for FY20e – FY22e

Acquisition of Deli Asia, Delisnacks, Dough Culture and Dough Heritage for about S$22 million for a 100% stake, boosting EPS of Koufu for FY21E by 11.7%. The four companies make up the Deli Asia group, one of Koufu’s biggest suppliers of fried food and dough products. Koufu will own 100% of Deli Asia Group post acquisition, based on Deli Asia’s unaudited pro forma net profit for FY2019, this is expected to add S$2.4m a year to Koufu’s net profit and is accretive to their EPS. The acquisition will be funded fully by internal resources. For FY20e, we have penciled in five months of earnings contribution from Deli Asia, subsequently providing for a full-year of contribution from FY21e – FY23e. At an implied acquisition multiple of 9.2x FY19 P/E, we view this acquisition positively.In our forward assumptions for Koufu’s EPS from FY21e – FY23e, we have not incorporated any synergies expected to accrue from the acquisition of Deli Asia, which provides for a potential uplift in earnings if the Group can realise synergies from the acquisition.

The Deli Asia Group’s complementary products and manufacturing processes will provide important synergistic effects for Koufu. Deli Asia has production facilities and a warehouse in Singapore in the manufacturing and storage of fried and partially fried food and dough products. These products are also highly complementary to the range of dim sum items Koufu is selling at F&B stalls in its foodcourts and coffee shops. Deli Asia licenses its Delisnacks brand to about 60 franchised stallholders at hawker centres and coffee shops that sell its food products at their stalls. In addition, under its Dough Culture brand, the group operates seven retail kiosks in Singapore at locations including suburban malls. These kiosks sell fried food and dough products such as banana fritters and related products such as Chinese desserts and drinks, directly to consumers.

Further cost synergies from the vertical integration of Deli Asia. The acquisition will enable the Group to accelerate its business expansion plan and diversify its income streams. We also expect the Group to gradually shift Deli Asia group’s production facilities for its fried food and dough products to the IF this year when it is completed. This will consolidate Deli Asia group’s food preparation and processing with Koufu’s own central kitchens to optimise economies of scale and operating synergies.

Crowds return post circuit breaker

Outlets at heartland areas show greater signs of recovery vs. outlets located within office vicinity post circuit breaker. We visited two of Koufu’s outlets at Square 2 @ Novena and Gourmet Paradise at Toa Payoh Central to gauge the size of the crowds during lunch hour on a weekday. We chose Koufu’s outlet at Square 2 @ Novena as this outlet caters mainly to the predominantly working-class group in the vicinity, while the Gourmet Paradise outlet at Toa Payoh Central was chosen as they serve primarily heartland residents.

At Koufu’s Square 2 @ Novena, we observed a healthy flow of patrons visiting the premises, with the average wait time for a table at about five minutes due to social distancing measures in place. We spoke to stall owners here, who indicate that their takings have improved to about 60 - 65% of sales before the circuit breaker measures kicked in. We think the improvement is encouraging, but the continued shortfall is expected to continue as the result of a significant number of office workers still working from home.

We also visited Koufu’s Gourmet Paradise outlet at Toa Payoh Central and observed significantly larger crowds here than what we observed at their Square 2 @ Novena outlet. We spoke to stall owners here who indicate that sales have improved to about 80 – 85% of sales pre-circuit breaker, which we think can be attributed to it’s proximity to the heartland areas. As a whole, we view the consumption recovery at the two outlets we visited as positive to the Group.

In a bid to combat the lower footfall, Koufu has also partnered with delivery platforms and launched delivery services within their own “Koufu Eat” App to boost online sales and sales for their tenants. When compared to third-party delivery platforms (like Deliveroo, Food Panda and GrabFood) their mobile application will enable tenants to save on the 20 – 25% commission fees charged by these platforms. While delivery is only available for Punggol and Sengkang region as at July 2020, overall online food ordering and deliveries have doubled since their launch according to the management.

Going forward, we expect more stallholders to sign up with Koufu’s app platform as well as third-party online delivery platforms as stallholders seek to diversify their takings and mitigate the effect of reduced footfall across the island. We think the logical next step for Koufu will be to roll out their delivery islandwide and support an even wider group of their tenants, increasing the stickiness of their offerings.

Valuation

We initiate coverage on Koufu Group with a BUY recommendation and a target price of $0.80. We peg Koufu to a PE of 18.5x FY21e, which is the average valuation of their peers (excluding Koufu) (Figure 24).

We think Koufu will benefit from the consumption recovery at their outlets as more people eat out, even though Koufu’s Elemen restaurants and Rasapura Masters food court at MBS will continue to be negatively impacted due to the continued restrictions on overseas visitors. We expect the Group’s move into the IF in 3Q2020 to be a major catalyst as the Group accrues cost savings through improved productivity and operational efficiency.

We view Koufu as best in class with a defensive business model and superior growth profile from their overseas expansion plans and the expansion of their new concepts (R&B Tea and their premium vegetarian Elemen restaurants). We like their historical record of generating positive free cash flow and forecast the Group to generate strong free cash flow of S$25m a year from FY20e to FY22e. Their strong balance sheet (FY19 net cash of S$86m or S$0.15 per share) puts them in good stead to ride out the current crisis as well as to take advantage of M&A activities to grow.

We think Koufu’s move to the IF in 3Q20 will see a potential re-rating for the Group as they begin to realise cost savings through increased productivity and operational efficiency. The larger central kitchen will decrease food preparation processes traditionally done on-site at F&B outlets. They will also be able to benefit from increased bargaining power with their suppliers through bulk orders purchase and central procurement. Lastly, we expect to see Koufu achieve better inventory management from the bigger storage and warehouse area.

Risks

Lease renewals for existing units and securing of new leases. Koufu leases substantially all of their F&B outlets in Singapore and Macau. Most of their existing leases have tenures of between three and four years at inception. The Group generally commence renewal negotiations with a landlord about six months before the expiry of each lease, and there is no certainty as to whether they will be able to renew their existing leases on favourable terms. In addition, on occasion, a landlord may, at the end of the tenure of the lease, put such premises up for open tender or solicit alternative bids. There is no assurance that they will be able to win such tenders or be more competitive than any alternative bids submitted. There is also no assurance that they will be able to win new tenders given the competitive nature of the industry.

Dependent on labour and foreign workers. Koufu’s business is labour intensive, and the Group relies on skilled and experienced personnel for their operations. The Ministry of Manpower (MOM) imposes policy instruments such as the imposition of levies and quotas, also known as dependency ratio ceilings, being the percentage of foreign employees permitted in a company’s total workforce. For the services sector, the dependency ratio ceiling has been lowered from the current 40% to 38% from January 2020 and 35% from 2021. A reduction in foreign labour quota without a corresponding improvement in their technological capability to reduce their reliance on foreign labour, will translate into higher costs for Koufu.

Failure to maintain an attractive tenant mix or maintain current occupancy rates. It is essential that their food courts, coffee shops and hawker centre maintain an attractive mix of stall operators that can offer customers a variety of F&B offerings and consistency in the quality of food and services. An unattractive mix of stall operators, or poor or inconsistent quality of food and services could result in customer dissatisfaction and a reduction in patronage of their food courts, coffee shops and hawker centre. There is also no guarantee that they will be able to sustain the current occupancy rates of their food courts, coffee shops and hawker centre, as this depends on their ability to manage their relationships with third party stall operators and the fees and rents charged to them. The sustainability of the hawker trade and availability of potential stall operators depend on the willingness of the younger generation to enter the hawker trade. This may also be affected by rising manpower costs, the size of the labour pool and an ageing workforce in Singapore.